A Monday Morning Musing October 14, 2019

A warrant is a common financial instrument designed to entice speculators’ participation in a company’s private placement. It grants the participant a fixed price option to acquire another share in the company at a future date. Private placement units commonly consist of a share and a half or full warrant with a one- to a five-year expiration date.

I opine that a warrant is a financial instrument that in the vast majority of cases has zero value. There are some obvious reasons why this is true and I detail them in the missive below.

But first, I present my own anecdotal evidence:

From 2013 to the present, I participated in 35 junior resource company private placements; 23 included an attached warrant. Five were private startups and five were shells, reverse takeovers, or spin-outs that came without a warrant. Two of the placements that had no warrant were secondary financings for an RTO and a spinco, and both were priced at significant discount to the market.

Folks, here’s the sad truth about these 23 warrant speculations:

So with hope and perhaps a prayer (if you are religious), the jury is still out on six warrants.

That said, of the 17 warrants that are said and done, only four were exercised and sold at a profit; that’s less than 25% winners!

Rest assured that I am not alone in my recent history of junior resource speculations. In several discussions with other professional speculators, we reached a general consensus that only one in every four or five warrants are in-the-money and exercised prior to expiry.

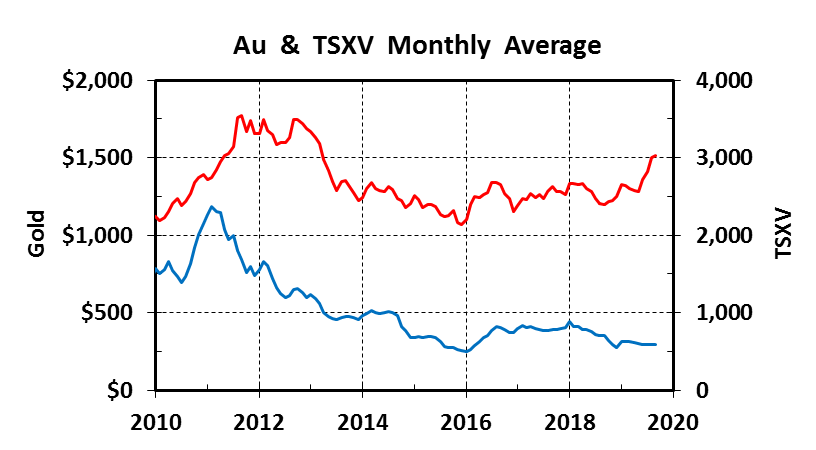

So let’s explore some reasons for this abysmal record. Certainly, macroeconomic factors have been important:

That said, the price of gold and the performance of the junior stock market are merely a part of this story.

I submit there is a fundamental flaw in the standard equity financing model and structure that demands private placement units include a share and a warrant. My reasoning is outlined below:

Folks, the gist is this: Private placement warrants seldom reward speculators with the opportunity they envision. Moreover, unexercised warrants often present a significant hindrance to a junior company’s share price, share structure, and future financial fortunes. .

At this juncture, I am only interested in early-stage financial opportunities in properly-constructed private startups, clean shell companies with well-constructed structures, and/or reverse takeovers of the above.

I assume significant risk with a five-plus month trading hold on every private placement. For the reasons outlined above, I do not want a warrant attached on the term sheet. If you really want to attract my hard-earned American dollars, I strongly suggest financing at significant discount to the market price.

To wit: Warrants are often the worst of wanton and wasted wagers and seldom have future value.

I will still consider a financing that features warrants but it must be a compelling story with a group of strategic investors who are demonstrably committed to the company and an orderly market that responds positively to exploration success.

Otherwise, for any story I like, I can purchase free-trading shares on the open market.

Ciao for now,

Mickey Fulp

Mercenary Geologist

The Mercenary Geologist Michael S. “Mickey” Fulp is a Certified Professional Geologist with a B.Sc. in Earth Sciences with honor from the University of Tulsa, and M.Sc. in Geology from the University of New Mexico. Mickey has 40 years of experience as an exploration geologist and analyst searching for economic deposits of base and precious metals, industrial minerals, uranium, coal, oil and gas, and water in North and South America, Europe, and Asia.

Mickey worked for junior explorers, major mining companies, private companies, and investors as a consulting economic geologist for over 20 years, specializing in geological mapping, property evaluation, and business development. In addition to Mickey’s professional credentials and experience, he is high-altitude proficient, and is bilingual in English and Spanish. From 2003 to 2006, he made four outcrop ore discoveries in Peru, Nevada, Chile, and British Columbia.

Mickey is well-known and highly respected throughout the mining and exploration community due to his ongoing work as an analyst, writer, and speaker.

Contact: Contact@MercenaryGeologist.com

Disclaimer and Notice: I am not a certified financial analyst, broker, or professional qualified to offer investment advice. Nothing in any report, commentary, this website, interview, and other content constitutes or can be construed as investment advice or an offer or solicitation or advice to buy or sell stock or any asset or investment. All of my presentations should be considered an opinion and my opinions may be based upon information obtained from research of public documents and content available on the company’s website, regulatory filings, various stock exchange websites, and stock information services, through discussions with company representatives, agents, other professionals and investors, and field visits. My opinions are based upon information believed to be accurate and reliable, but my opinions are not guaranteed or implied to be so. The opinions presented may not be complete or correct; all information is provided without any legal responsibility or obligation to provide future updates. I accept no responsibility and no liability, whatsoever, for any direct, indirect, special, punitive, or consequential damages or loss arising from the use of my opinions or information. The information contained in a report, commentary, this website, interview, and other content is subject to change without notice, may become outdated, and may not be updated. A report, commentary, this website, interview, and other content reflect my personal opinions and views and nothing more. All content of this website is subject to international copyright protection and no part or portion of this website, report, commentary, interview, and other content may be altered, reproduced, copied, emailed, faxed, or distributed in any form without the express written consent of Michael S. (Mickey) Fulp, MercenaryGeologist.com LLC.

Copyright © 2019 Mercenary Geologist.com, LLC. All Rights Reserved.

Significant copper and molybdenum intersections include: HM09: 13... READ MORE

Aya Gold & Silver Inc. (TSX: AYA) (OTCQX: AYASF) is pleased t... READ MORE

Key Highlights – Preliminary Economic Assessment Pre-Tax Net Pr... READ MORE

Aris Mining Corporation (TSX: ARIS) (NYSE-A: ARMN) announces its ... READ MORE

Orla Mining Ltd. (TSX: OLA) (NYSE: ORLA) announces the results fo... READ MORE