A $20-million gold explorer with a small, high-grade gold deposit in Red Lake, Ontario, shot up to $160 million in April when it inked a deal to buy the newly built (but failed) Madsen gold mine for $18.5 million.

The price was a song for an asset with 2 million ounces of high-grade gold in reserves, a brand-new process plant, and kilometres of underground development. That’s what you can get if you’re willing to buy a mine that failed within 19 months of first production.

The deal stood out because it was a team taking on the risk – and opportunity – in a failed mine. It also stood out because Frank Guistra stepped forward to back

West Red Lake Gold Mines (TSXV: WRLG).

Guistra is one of the most successful mining entrepreneurs in Canadian history, having built or led several leading mining merchant banks and guided Wheaton River Minerals to become the prize company that Goldcorp bought in 2005 to become the major miner it is today.

He had stepped away from mining in the last decade to focus on philanthropy…but in the last year he returned. With decades of successful experience investing in gold and commodities, Guistra thinks now is a prime moment to invest in today’s beaten-down gold sector.

West Red Lake Gold is one of his top picks. That Guistra bought 12% of the company gave other investors confidence this team could turn the failed Madsen mine around.

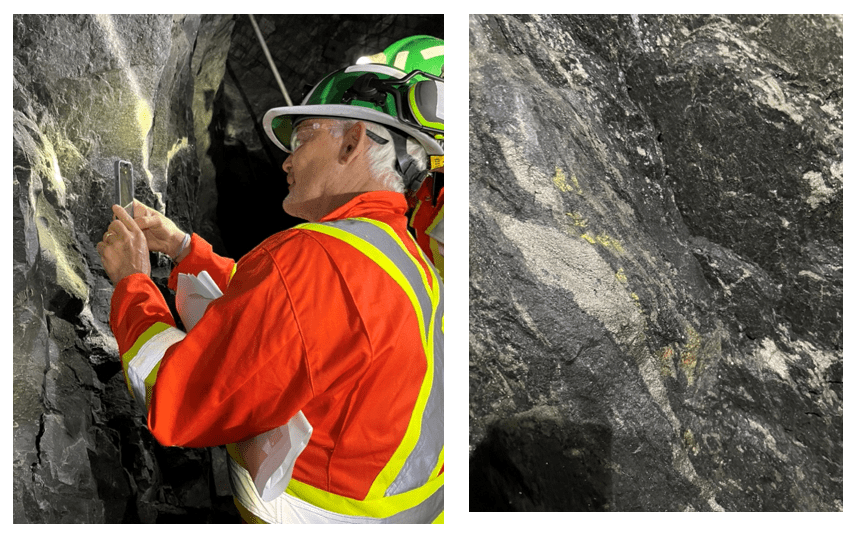

Frank Guistra taking photos of gold in the rocks at the Madsen mine, like the photo on the right that I took.

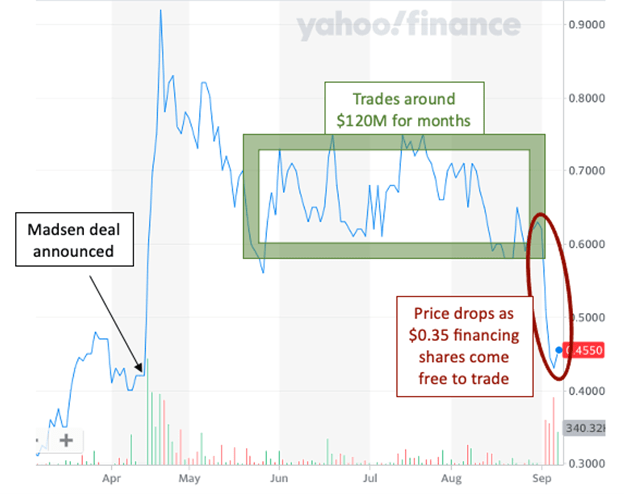

That confidence propelled WRLG’s shares as high as $0.90 following the deal. Meanwhile, WRLG was completing a financing at $0.35 per share. It was a very popular financing; most participants only got a third of the allocation they requested.

WRLG eased back some and then traded reliably between $0.60 and $0.75 for four months…until last week, when the price dropped.

There was no news, no corporate disappointment. The story is moving ahead in all the right way. So why the price drop?

Because that $0.35 financing came free to trade on Monday and some financing investors are selling to lock in a double.

It’s a very common pattern. Company raises money at $A. The share price rises to $B over the next few months but financing investors cannot sell because financing shares are locked down for four months. Once they can be traded – once the free trade date hits – the share price often declines right back to $A as financing investors lock in gains.

The thing is, even though it’s a common pattern, free trade date price drops are often misunderstood. Anyone new looking at the share price chart will just see a big decline and assume something bad happened.

But in the case of WRLG, it didn’t. That means this free trade date price dip is an opportunity to buy a stock that Frank Guistra and a strong team of geologists, mine engineers, and mining capital markets operators are backing in a big way.

That’s the main message I want to send today: that West Red Lake Gold Mines dropped because of a free trade date, not a project or corporate problem. That means this price dip is an opportunity to buy a stock with a clear and low-cost pathway to production and growth in one of the world’s most storied gold mining districts, at a brand new mine bought for pennies on the dollar with backing from an experienced and monied group.

This group is backing West Red Lake Gold in a big way because they think the Madsen mine

- Can become a strongly profitable mine in short order by implementing a few key fixes and not being burdened by hundreds of millions of dollars in construction debt

- Can be a processing hub for stranded deposits in the area. Red Lake is famous for high grade gold but small deposits aren’t enough to build a mine around. Sending ore from those deposits to an already built and proven mill could unlock value.

- Can, with a robust mine plan and clean execution, drum up the same kind of market excitement that lifted the previous owner past $1 billion valuation

To explain why WRLG thinks it can fix the mistakes made at Madsen, let me run through the backstory.

| Pure Gold built the Madsen mine in 2020-2021. The market loved it: a Canadian company building a new high-grade gold mine in Red Lake, the most storied gold district in Canada. As construction finished and the mine started up, Pure Gold’s valuation bested $1 billion.

A year later it was down 78% as the mine struggled to access enough good ore and the company struggled under a heavy and restrictive debt load. In October 2022, 19 months after starting up, the mine was put on care and maintenance.

Six months later West Red Lake Gold Mines bought the Madsen Mine, in which $350 million had been invested, for $18.5 million in cash and shares.

It’s an amazing deal…if they can make Madsen work.

WRLG is confident it can because it was corporate decisions about how to finance the build that sunk the mine. It did not fail because the gold wasn’t there; it did not fail because the mill was faulty. Madsen failed because of financial decisions.

There were two categories of financial decisions that failed. They were related and made each other worse.

First, to make the asset more appealing to potential buyers, Pure Gold thought it was important to keep the mine free of royalties and to limit equity raises. So they relied on debt for construction capital.

Second, limiting themselves to debt meant they were tight on cash from the start. To make that work they cut corners and pushed some big costs out into the operating budget, to make the build price smaller.

Relying on debt, cutting construction corners, and pushing costs into the future worked together to sink the company.

Things that would have increased the mine’s odds of success were not done, like sufficient infill drilling in the early ore areas, developing down to deeper and richer parts of the deposit, and building enough underground infrastructure to get ore to the surface efficiently.

Not doing those things made the mine falter. And if a mine carrying lots of debt falters, it can quickly run up against its debt covenants. Debt covenants limit what a borrower can do. They can be as simple as a repayment schedule or as involved as a max debt-to-asset-value ratio. When a new mine stumbles, it is very easy for a borrower to trip these covenants.

Recovering from such trips is very difficult because what a struggling new mine needs to succeed is more investment, which is exactly what a company can’t provide when its new asset is faltering and debt collectors are calling.

Pure Gold’s news releases tell this story. In April 2022, five months into production, the company announced a month-long vacation from debt covenants to give it time to cut costs at the mine (“reduced headcount, rationalized equipment, and optimized underground development initiatives are expected to lead to an approximate 30% reduction in costs in Q2 compared to Q1”) while increasing production.

If spending less but producing more at a new mine that’s not working very well seems impossible, that’s because it is. And then Madsen failed. |

|

| The cynic in me wondered if this why-Madsen-failed story was too simple. So I visited the mine in July. The most important trip takeaway came from all the people who worked at Madsen during Pure Gold’s tenure. Everyone who was there through the build, ramp up, and failure supported and fleshed out WRLG’s telling of what went wrong. |

|

Heading underground with WRLG advisor Rob McLeod

Let me give you a few examples.

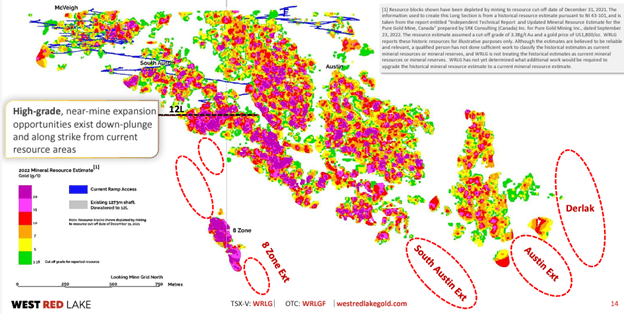

One of the bigger problems was where they chose to mine. The gold at Madsen sits in blobs along two parallel structures. In the block model below, red and purple are high grade; green and yellow are low grade. The good stuff is deeper, as you’d expect since this deposit was mined in the 1960s.

Pure Gold’s first plan was to start mining the good stuff in the middle of the image, in the middles of the parallel Austin and South Austin zones.

To get to those areas required substantial tunnelling. They started that work; it’s the blue squiggle on the right side, known as the East Decline. But then they found the McVeigh zone, which they thought offered enough good-enough material to carry the mine in its first years. So they abandoned the East Decline and started a second tunnel directly into McVeigh.

| Getting to ore faster might seem like a good idea…but grade is king. McVeigh is not nearly as rich as Austin and South Austin, so the material coming to the mill was lower grade than the feasibility study had assumed. That is always a bad starting point.

At least they had two tunnels though, right? Sure…except that they abandoned the East Decline because it was expensive to develop two tunnels. And when they pushed the West Decline through McVeigh into South Austin, they were left with only one way for people and machinery to go into and out of both mining areas. Underground traffic jams are very bad for mining efficiency.

That’s the short version of what went wrong underground. And on surface the problems really piled up.

Mine Engineering 101 says you drop and pick up ore as little as possible, ideally only once or twice. A series of cost-saving decisions, like not driving a short tunnel under a public road and using a loader 24 hours a day to feed ore into the crusher because they didn’t buy a vibrator for the automated mill feeder so it didn’t work, meant Madsen ore was dumped and reloaded 5 or 6 times.

That is crazy expensive and slow. And when the ore in question has significant free gold, gold literally falls out every time ore is dumped and reloaded. So they wasted time, added cost, and left gold all over the ground.

COVID didn’t help. Between cutting corners on spending and COVID creating long equipment wait times, workers were constantly scrambling to keep things going. A lack of core drills meant they needed to use air core rigs for underground drilling, which required a fleet of diesel air compressors, which were very expensive to run and maintain (especially through winter). Examples like that abound.

It all meant grades were much lower than planned and operating costs were out of control.

I just spent hundreds on word slamming Pure Gold’s approach. Approach comes from the top; mine workers take direction and do their best to make an operation work. And the Madsen team almost had it. By the time Pure went under the mill was processing 800 tpd, recoveries were good, and the mine had just enough active stopes to feed the mill. |

|

| WRLG scored a heck of a deal buying Madsen for $6.5 million cash and $12 million in shares (plus up to $10 million in payments down the road). The mill is new and proven, there are 2 million ounces of high-grade gold in the ground, there are extensive underground workings (including a deep historic shaft that could be refurbished to hoist ore for a few million dollars), and there is ample opportunity to find more gold.

The potential to make Madsen a profitable gold mine of scale is readily apparent. It will take some work.

They are drilling to upgrade resource confidence and making a robust mine plan. They will fix the inefficiencies on surface: drive that tunnel under the road, buy a primary crusher, and set up to feed ore into that crusher efficiently.

They are working satellite opportunities. The project WRLG already owned next door, Rowan, hosts a million ounces of high-grade gold in a steeply dipping deposit starting at surface. WRLG is drilling there now with great success – looks like Rowan will get bigger and better – and doing the environmental studies to permit a satellite mine there.

The Wedge zone at Madsen is similar – a high-grade gold zone at surface with the potential to juice grade through the Madsen mill – and WRLG just started drilling there. WRLG will show how these satellite operations could benefit the mine by planning them as PEA-level expansions alongside a new pre-feasibility study for Madsen early next year.

WRLG held a valuation around $120 million before free trade date selling pulled it back to $84 million. It has about $10 million in the bank to put into the mine, plus $7 million in exploration capital to drill at Rowan and Wedge.

The company will finance again this year to fund some $30 million worth of work in 2024, including a whack of underground development, potentially refurbishing the shaft, and implementing those mill fixes.

They’ll raise some of that this fall and then issue a PEA for the restart in Q1. That will be an important document, as it will tell the market what to expect from Madsen and when. Then WRLG will do all the drilling and engineering and reserve modeling and mine planning and satellite deposit permitting needed for a robust restart.

I left the site visit confident this team will make Madsen work. Getting that work done will give the market the kind of confidence I got by visiting the site.

I see two levels of opportunity here.

First: buying for the Free Trade Date rebound.

WRLG is getting out to tell the Madsen story over the next month. They don’t want this Free Trade Date slide to persist. So there’s a short-term opportunity there.

Second: buying for what Madsen will be worth when it restarts.

I can’t pin a value on that as a lot of big questions (scale and grade, for instance) aren’t yet answered, but there’s somewhat of a test case in Rubicon Minerals.

Rubicon failed spectacularly in building the Phoenix gold mine in Ontario. The company went bankrupt, restructured, changed management and the mine plan completely, tried again and got the mine going nicely, and got acquired by Evolution Mining for $350 million.

Madson and Phoenix are both high-grade Red Lake gold deposits but they failed for different reasons. (Rubicon rushed into building without sufficient knowledge of the deposit.) But even though they’re different, I see a parallel in how Battle North (the name Rubicon took on after bankruptcy) rose from near-zero valuation to a $350-million takeout: by fixing the errors in a new mine without being burdened by huge construction debt.

West Red Lake Gold isn’t a story that is going to race ahead. But it is a deal with strong potential to create significant new value from a mine that failed for reasons that can be fixed in the right hands. And will attract all kinds of attention if the gold market rises for its high grades, near term production, Guistra backing, and storied setting. |

|

| Courtesy of the Resource Maven |

|