New Pacific Metals Corp. (TSX: NUAG) (NYSE-A: NEWP) is pleased to report the results of its updated preliminary economic assessment technical report titled “Carangas Project NI 43-101 Technical Report and Preliminary Economic Assessment” for the Carangas project in Oruro Department, Bolivia prepared in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects by Ausenco Engineering Canada ULC dated effective July 16, 2026. The Updated Carangas PEA Technical Report considers an increased throughput rate and the inclusion of the gold zone when compared to the previous Preliminary Economic Assessment technical report dated September 5, 2024. Highlights from the Updated Carangas PEA Technical Report are as follows (all figures in US Dollars):

The Project has robust economics, manageable upfront capex, annual silver production of approximately ten million ounces per year, and over one million ounces of gold produced over the life of mine. With the completion of the Updated Carangas PEA Technical Report, the Company will continue to advance technical work, including a 30,000 meters infill drilling program. Besides the technical works, the Company will also focus on advancing the Project’s permitting front aiming to complete the Exploration Licenses to Administrative Mining Contracts conversion and to start the Environmental Impact Assessment Study process over the remaining periods of the year.

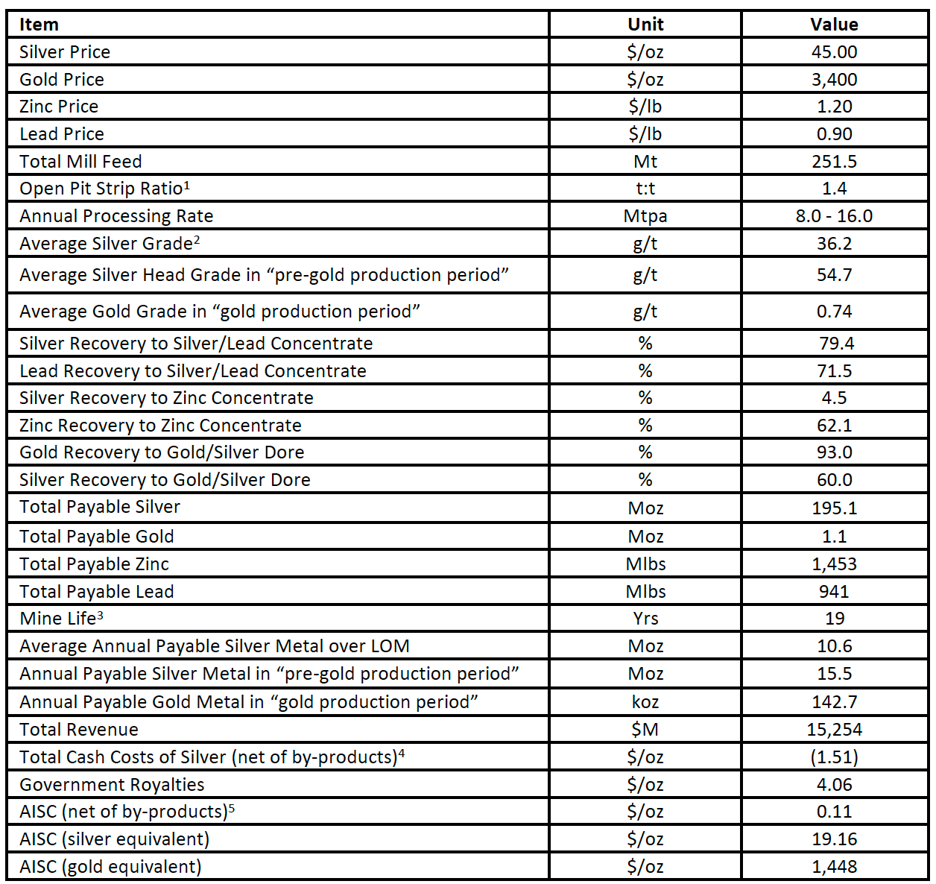

Economic Results and Sensitivities

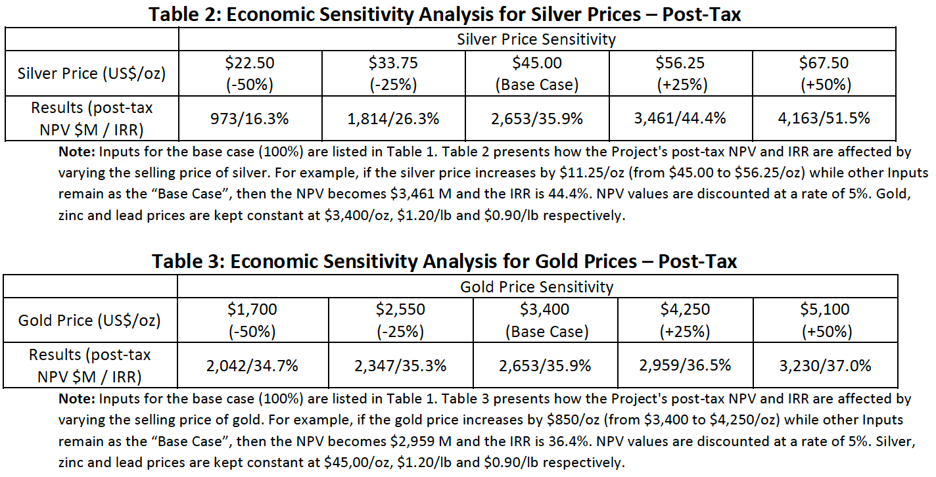

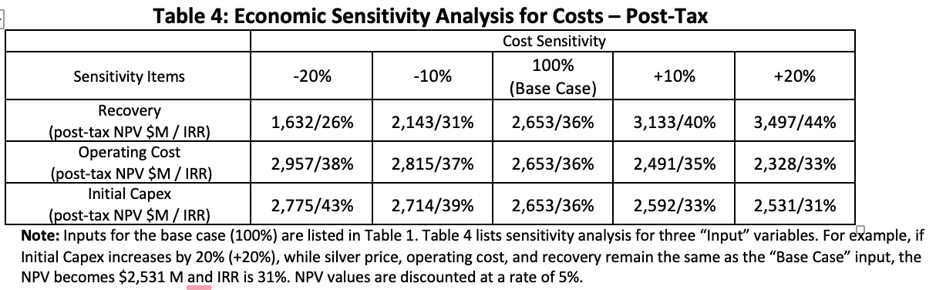

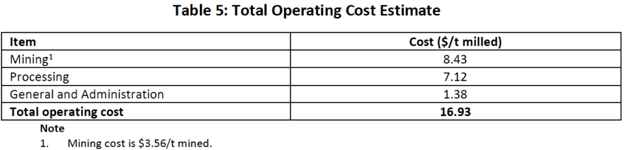

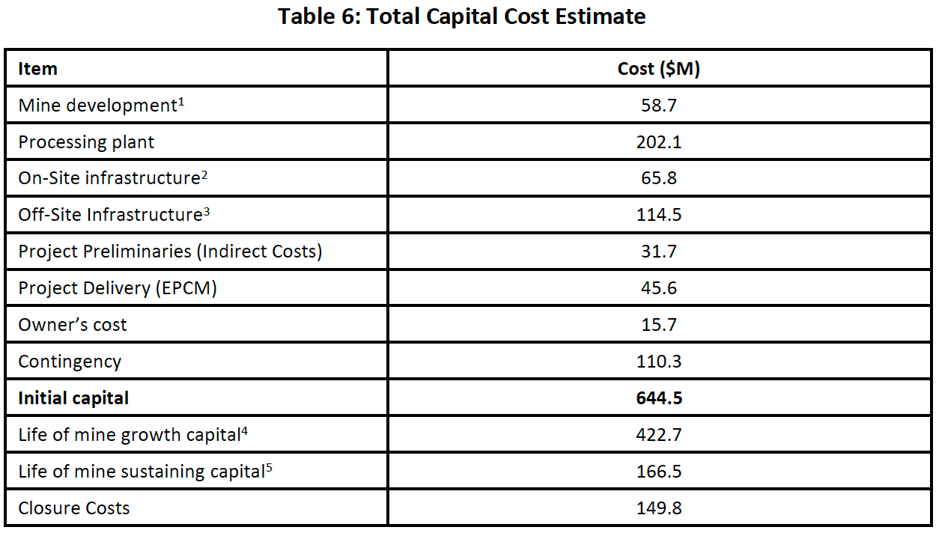

Table 1 shows key assumptions and summarizes the projected production and economic results of the Updated Carangas PEA Technical Report. Tables 2 and 3 show sensitivities to silver and gold prices and Table 4 shows sensitivities to operating and capital costs.

[1] AgEq is calculated using: AgEq Oz = Ag Oz + Au Oz x (Au Price/Ag Price) + Zn lbs x (Zn Price/Ag Price) + Pb lbs x (Pb Price/Ag Price), metal prices shown in Table 1

Notes

Capital and Operating Costs

The Project, as outlined in the Updated Carangas PEA Technical Report, is anticipated to include contract mining open-pit operation, supplying mill feed to a conventional crushing, grinding and flotation circuit, which is expected to produce silver-lead and zinc concentrates. The operation is expected to be expanded from 8.0 million tonnes per year to 16.0 Mtpa in year 6 by the addition of a twinned crushing, grinding and flotation circuit. In year 9, it is expected that an 8.0 Mtpa gold circuit (including cyanide leaching, counter-current decantation, Merril-Crowe, and smelting) will be put into operation. This circuit will make use of the crushing, grinding and rougher flotation units from the second concentrator plant. It is expected that the initial concentrator plant will continue to operate at 8.0 Mtpa producing silver-lead and zinc concentrates. The Updated Carangas PEA Technical Report anticipates the Project will have several capital and operating cost advantages:

Note

Mining

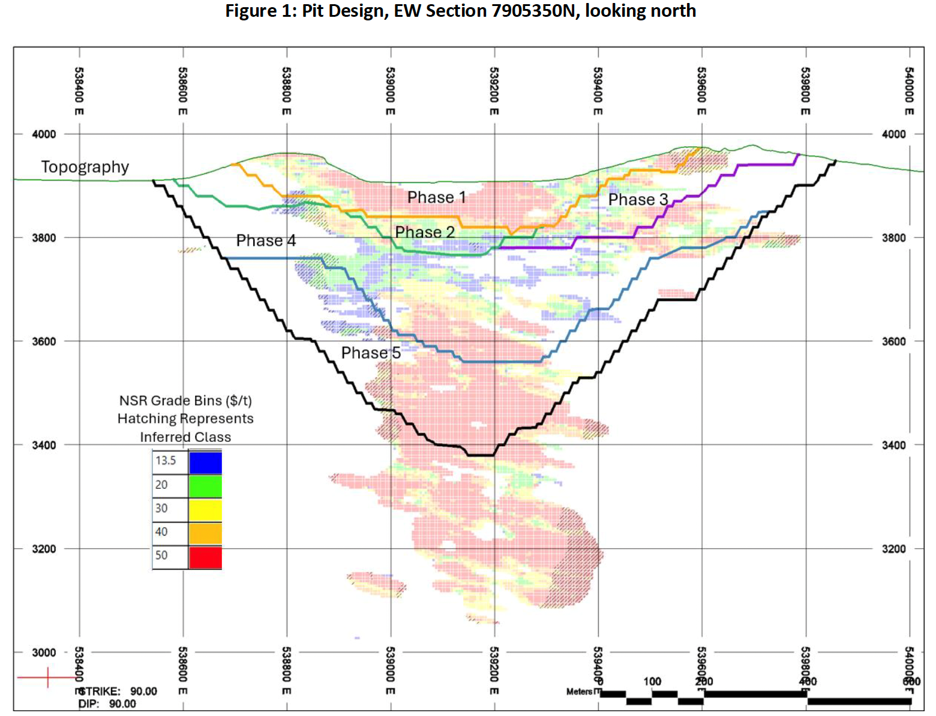

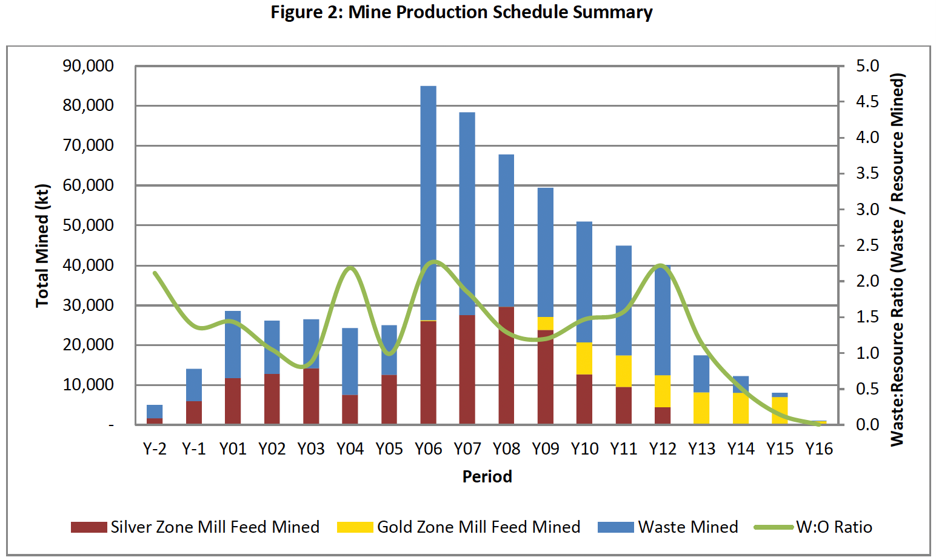

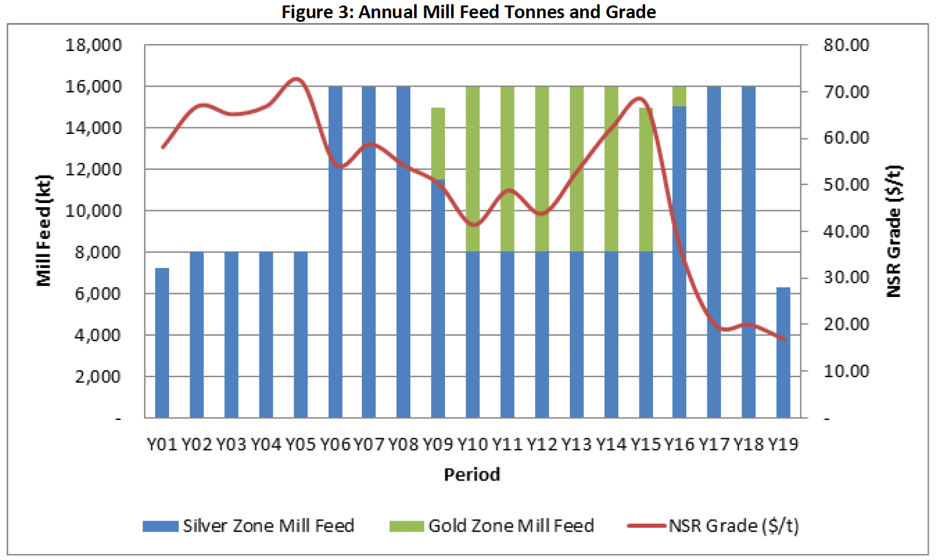

It is anticipated that the deposit will be mined using a conventional open pit approach. This entails drilling and blasting, with loading by hydraulic excavators and haulage by off-highway rear dump haul trucks. A SW-NE cross section showing the resource model grades and pit is illustrated in Figure 1. The mine production schedule is illustrated in Figure 2.

Mill feed tonnes and grade are a subset of the Mineral Resource Estimate, accounting for planned mining dilution and recovery. A mining net smelter return cutoff grade of $13.50/t is applied and all mined material below this cutoff grade is treated as waste. The mining cutoff grade is chosen to cover process and G&A operating costs for the Project.

The Updated Carangas PEA Technical Report assumes that mill feed will be hauled to the primary crusher or a run-of-mine stockpile near the crusher. A portion of the oxides and lower grade resources mined in the early years are planned to be stockpiled east of the open pit and processed over the life of mine. Waste rock will be hauled to waste storage facilities north of the open pit or to construct the tailings storage facility dam, further north of the open pit. It is anticipated that mine operations will be conducted by a contractor with current operations in Bolivia.

It is anticipated that open-pit mining will commence in the first year of construction. The mine plan anticipates that 19 Mt of waste and oxide material will be mined, over a two-year pre-production period. Peak open-pit production is expected to be 85 Mt per year. The planned open pit contains a total of 615 Mt of material (mineralized material and waste) which is scheduled to be mined out by Year 16 of milling operations. 105 Mt of oxide and lower grade material is planned to be stockpiled throughout the life of mine, with years 16-19 processing stockpiles exclusively. The stockpiled oxide is rehandled to the mill over the life of mine, targeting 13% of the overall silver zone mill feed.

Notes: Net Smelter Prices and metallurgical recoveries are used to define the NSR cutoff grade. NSPs include market price assumptions of $40.0/oz Ag, $3,200/oz Au, $0.90/lb Pb, $1.20/lb Zn. Various smelter and refining terms, offsite costs, and a 5% royalty (6% for Ag) derive NSPs of $17.5/oz Ag in Zn concentrate, $34.4/oz Ag in Pb concentrate, $34.8/oz Ag in doré, $3,028/oz Au in doré, $1,070/t Pb, and $1,270/t Zn. Metallurgical recoveries of 6% Ag in Zn concentrate, 81.6% Ag in Pb concentrate, 60.4% Ag in doré, 93.4% Au in doré, 2.3% Pb in Zn concentrate, 73.4% Pb in Pb concentrate, 66.9% Zn in Zn concentrate, and 21.9% Zn in Pb concentrate are applied. The metal prices, smelter terms, and recoveries for the economic analysis are slightly different from the values described here. Checks have been made by the qualified person to ensure that the mine plan would not be materially altered by revising these inputs to the metal prices used to evaluate the project economics in the Updated Carangas PEA Technical Report.

Mineral Processing

The Project is designed to process 8.0 Mtpa of mineralized material in the first 5 years, and 16.0 Mtpa in years 6 to 18. The overall mill production schedule is illustrated in Figure 3. The processing facility will use conventional comminution circuits followed by selective sequential flotation to produce a lead/silver concentrate and a zinc/silver concentrate. These circuits will include primary crushing, followed by a SAG-Ball milling circuit and sequential selective flotation to separate silver/lead and zinc while rejecting pyrite and non-sulfidic gangue minerals. During years 9 to 16, the gold plant will use convention cyanide leaching for the gold flotation concentrate along with CCD, Merrill Crowe, and smelting circuits to produce gold doré. Tailings would then be thickened and pumped to a conventional storage facility.

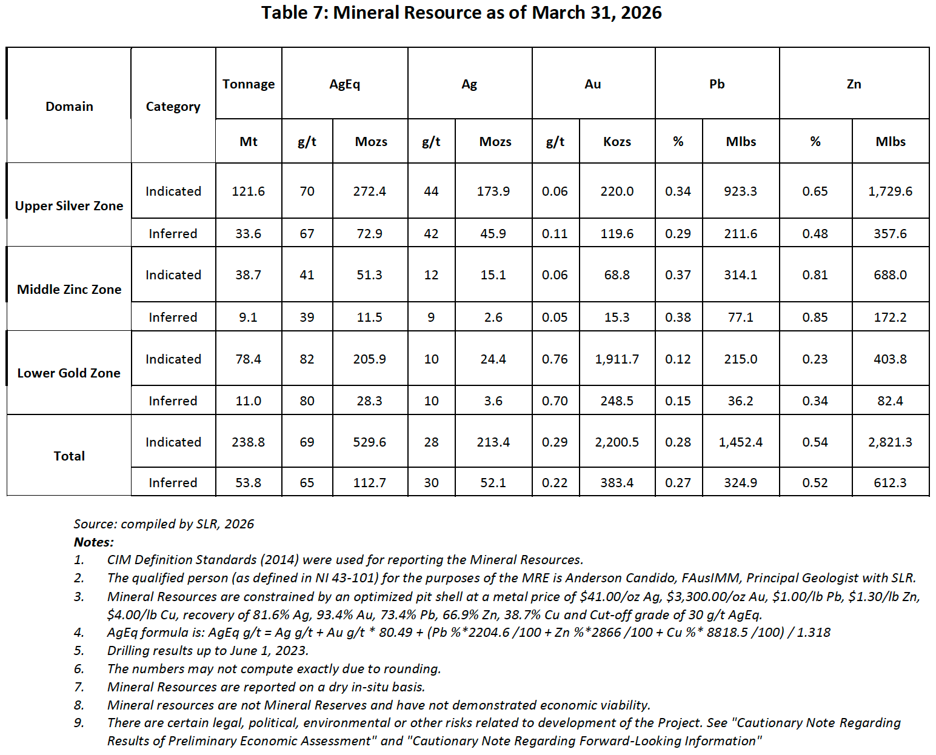

Mineral Resource Estimate

The MRE, constrained by a conceptual open‑pit shell for reporting purposes, is reported using a cut‑off grade of 30 g/t AgEq and is presented in Table 6 with an effective date of March 31, 2026.

Next Steps

The strong economics shown in the Updated Carangas PEA Technical Report warrant New Pacific continuing to advance both the technical and permitting aspects of the Project. Recent progress has been made with the local community including the signing of a framework community agreement earlier this year (see press release dated February 23, 2026), as well as successfully completing a prior consultation on July 6 to obtain community and other regional stakeholders’ consent as part of the requirements for the conversion of the Carangas ELs to AMCs. The application process for the ELs to AMCs conversion started in 2025 and all required documents have been submitted to the Bolivia’s Ministry of Mining and Metallurgy since then. With the recently completed prior consultation, the Company expects that the remaining administrative work and legislative approval of the conversion of the ELs to AMCs could take up to six months.

With the progress made on obtaining the AMCs, the Company plans to begin a 30,000 metre drilling campaign at Carangas in September 2026. Approximately 25,000 metres of drilling will be focused on converting inferred resources to indicated resources, with the balance of the drilling testing the Carangas gold zone for possible extensions and new step out targets. As part of this work, the Company will also gather samples for feasibility level metallurgical test work and conduct geotechnical and hydrological drilling.

Once the AMCs are obtained, the Company will start the application to obtain its environmental categorization as a proposed open pit operation from Bolivia’s Ministry of Environment and Water, formally commencing the EEIA process. Work will also commence on gathering baseline environmental and social data as well as other associated technical work to fulfill the requirements of the EEIA. It is expected that this work will be completed by the end of 2027.

Qualified Persons

The qualified persons for the Updated Carangas PEA Technical Report are Mr. Anderson Candido, FAusIMM, Principal Geologist with SLR Mr. Jinxing Ji, P.Eng., Metallurgist with JJ Metallurgical Services, Mr. Kevin Murray, P.Eng., Principle Process Engineer with Ausenco Engineering Canada ULC (“Ausenco”), Mr. Scott Elfen, PE, SME, and Global Technical Lead (Geotechnical) with Ausenco, Mr. James Millard, P.Geo., Director Strategic Projects with Ausenco, and Mr. Marc Schulte, P.Eng., Mining Engineer with Moose Mountain Technical Services. The specific sections for which each qualified person is responsible will be outlined in the Updated Carangas PEA Technical Report. All such qualified persons have reviewed and verified the technical content in this news release relevant to the sections of the Updated Carangas PEA Technical Report for which they are responsible. The qualified persons have verified the information disclosed relative to the sections they have responsibility for in the report.

Further details, including risks and uncertainties will be included in the Updated Carangas PEA Technical Report which will be posted under the Company’s profile at sedarplus.com within 45 days of this news release.

This news release has been reviewed and approved by Alex Zhang, P.Geo., Vice President of Exploration of New Pacific Metals Corp. who is the designated qualified person for the Company.

About New Pacific Metals

New Pacific is a Canadian exploration and development company advancing two permitting stage precious metals projects in Bolivia. Its Silver Sand project in Potosí has the potential to become one of the world’s largest silver mines. The Carangas Silver–Gold project in Oruro strengthens the Company’s portfolio through scale, robust economics, and regional exploration potential. With near a decade of operating experience in Bolivia, New Pacific has earned the confidence of its stakeholders and shareholders.

Canadian Copper Inc. (CSE: CCI) announces that it has closed its ... READ MORE

Thunder Gold Corp. (TSX-V: TGOL) (FSE: Z25) (OTCQB: TGOLF) is ple... READ MORE

5.17 g/t Au Over 2.9 Meters and 7.37 g/t Au Over 2.0 Meters VI... READ MORE

Abcourt Mines Inc. is pleased to present a major, unaudited opera... READ MORE