Commodity analysts predictions are usually wrong about copper supply, often predicting a glut in the market for the ubiquitous metal used in everything from piping and wiring in houses, to components of electric vehicles.

Elusive surplus

In 2022, copper mine output increased by 4% to 21.9 mln t and refined copper production by 1% to 24.6 mln t. Global refined copper consumption totalled 24.8 mln t.

When the International Copper Study Group (ICSG) met last October, it was expecting a market surplus of 155,000 tonnes in 2023. In May, the group changed that to a 114,000-tonne deficit.

The first thing we notice from this statistic is its relative small size. In a total copper market of 22 million tonnes, we had an immaterial deficit of 114,000 tonnes, considerably less than 1% of the overall market. Can anyone really claim to be so accurate as to predict the amount of surplus or deficit to within the equivalent of less than a 1 tonne in a hundred? What is basically a rounding error? It seems highly unlikely.

But for the sake of argument, let’s say the ICSG’s deficit forecast for 2023 is correct. What accounts for the missed target?

Reuters’ metals columnist Andy Home points to two strands in the current copper narrative. One is that China’s copper usage is growing faster than previously forecast. Second is that mine supply has once again failed to live up to expectations.

The ICSG reports China’s apparent usage of refined copper is expected to increase by 1.2% this year and 2.4% in 2024. Usage growth in the rest of the world is anticipated to beat last year’s 0.4% pace @ 1.6% this year, surpassing pre-covid levels, according to the ICSG.

The group contends that despite challenging macroeconomic conditions, “manufacturing activity is expected to continue rising in most of the key copper end-use sectors”.

The more interesting numbers relate to mine supply. When the ICSG met last October, it expected global mine production to surge by 3.9% in 2022 and 5.3% this year. At the time of Home’s article, in May, the group thought mine output growth last year was 3%, and it cut its forecast to 3% this year.

Remember, new copper supply is concentrated in just five mines — Chile’s Escondida, Spence and Quebrada Blanca, Cobre Panama and the Kamoa-Kakula project in the DRC.

Home references four of them, all except the biggest copper mine in the world, Escondida @ 1 million tonnes per year, as supply additions that have been ramping up simultaneously.

However, the expected wave of new supply is being offset by multiple hits to existing operations.

The ICSG cites as reason for its lowered mine growth expectations “operational and geotechnical issues, equipment failure, adverse weather, landslides, revised company guidance in a few countries and community actions in Peru”.

The Group and every other copper analyst include a supply disruption offset in their mine supply forecasts but the past six months have been particularly problematic even by copper’s historical standards of mine under-performance.

The net effect is a smoothing of the supply wave over the forecast period with mine growth expected to slow to 2.5% in 2024 as current ramp-ups are completed and any new additions arrive late in the year, according to the ICSG.

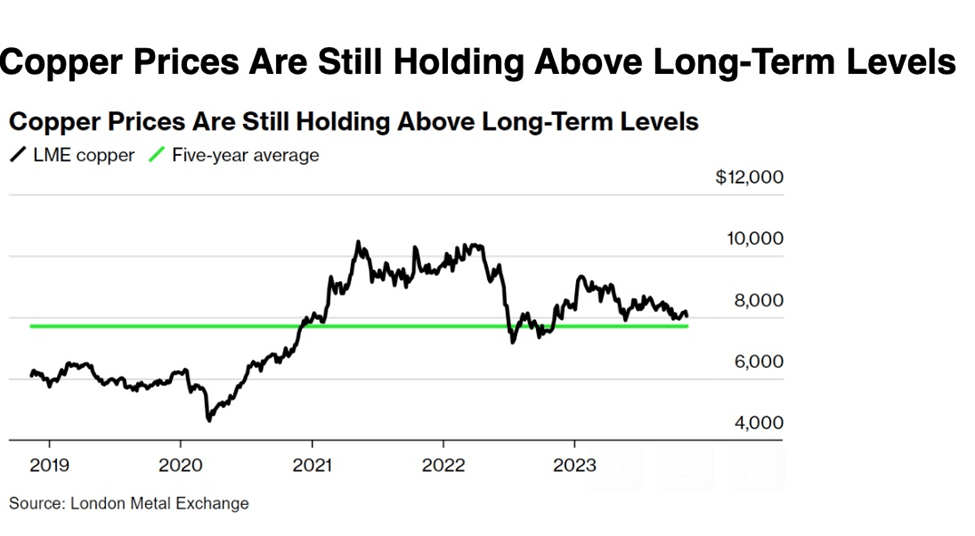

Home’s analysis also points to a dispute in the current copper narrative between bulls and bears. The bulls represented by Goldman Sachs think there is “now no new supply wave this year” and warns of a “stock out episode” as inventory levels are drawn down to critical levels.

The bank therefore targeted a 25% increase in the copper price this year, with a 12-month forecast (from May) of $11,000 per tonne.

On the bear side is Citi, with the investment bank declaring “A copper stock out is extremely unlikely in 2023 in our view.” Citing weak global demand, high finished goods inventories and improving supply, Citi downgraded its price forecast from May to July from $8,500 to $8,000 per tonne.

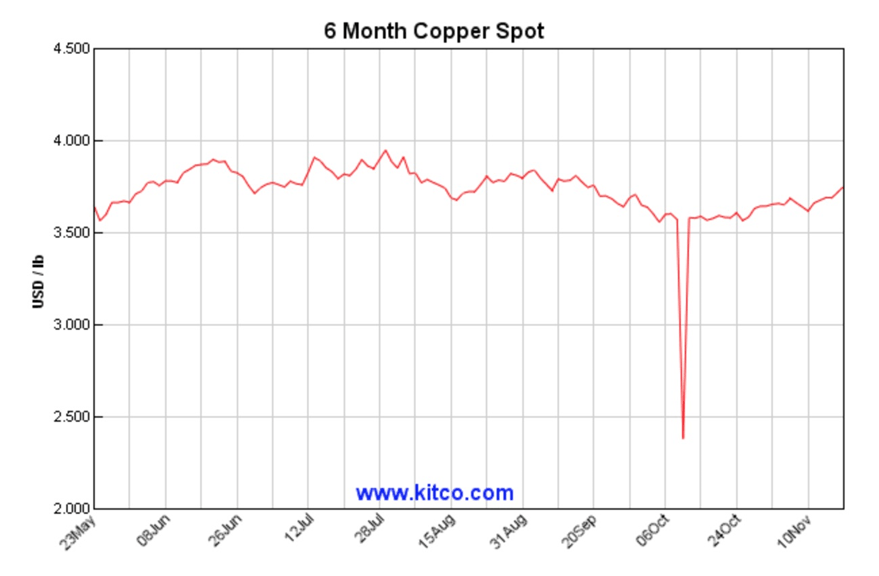

Kitco’s 6-month chart shows spot copper trading between a low of just under $2.50 a pound ($5,511 per tonne) in early October to nearly $4/lb ($8,818/t) in late July.

Source: Kitco

Prices rose on Monday due to growing optimism for an end to the Federal Reserve’s rate hikes, with December copper futures hitting $3.81 per pound on the Comex in New York.

Source: London Metal Exchange

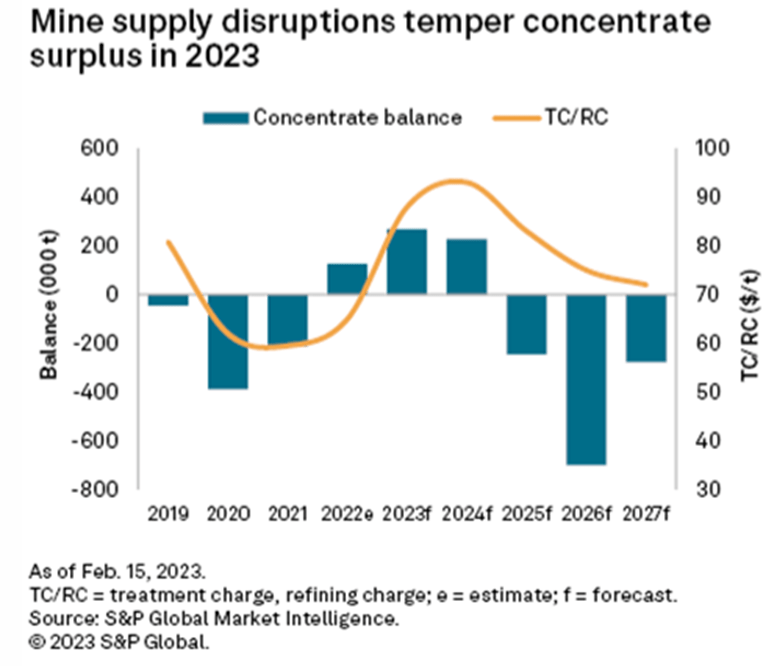

Smelter fees

While Citibank achieved a more accurate 2023 copper price forecast than Goldman Sachs, by one important metric its supply optimism for 2024 is wrongly placed.

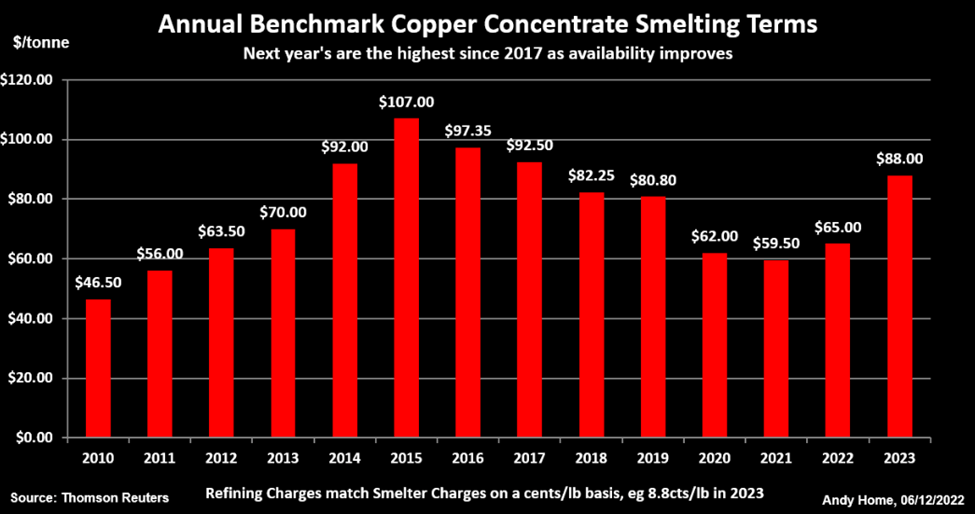

Every November, global copper miners and Chinese refineries meet to negotiate their copper concentrate contracts and settle treatment and refining charges (TC/RCs) for the following year.

Miners pay smelters a fee to process copper concentrate into refined metal, to offset the cost of the ore. TC/RCs fall when tight concentrate supplies squeeze smelters’ profit margins.

“Smelter charges for converting mined concentrate to refined metal offer a mirror on what is happening at the raw materials stage of the copper supply chain, rising during times of surplus and falling during times of deficit.” Reuters

If we are heading into a surplus in 2024, as Citibank sees it, why are smelter fees falling?

Last week Bloomberg reported that Antofagasta, a Chilean miner, and Jinchuan Group, a Chinese smelter, agreed to set 2024 treatment and refining charges 9% lower than this year, “as the supply of mined ore tightens and refining capacity expands.”

The charges, of $80 per ton and 8 cents per pound, compare to a six-year high of $88/t and 8.8 cents/lb in 2023, and are the first decline in fees in three years.

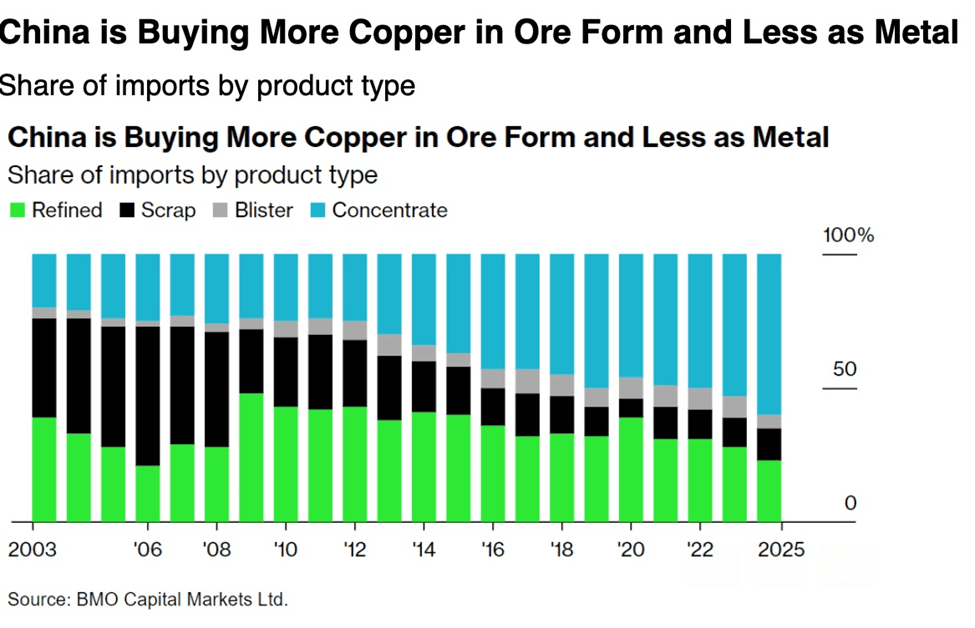

Readers of last week’s AOTH article will recall that to ensure self-sufficiency, China is/ has expanded its network of copper smelters, meaning it will start to import much more copper ore for processing domestically.

“Like all countries, China sees a strategic need for copper — particularly now with the growth in green energy applications — and China like other countries wants to ensure self sufficiency,” said Craig Lang, principal analyst at researcher CRU Group.

“China will account for about 45% of global refined copper output this year, according to CRU.” Bloomberg

China’s new copper smelting capacity is expected to turn China into a net copper exporter by 2025 or ‘26. With so many smelters requiring copper concentrate, the market for concentrate is tightening.

Deficit looms

As is the entire copper market. In February CNBC reported that “a copper deficit is set to inundate global markets throughout 2023, fueled by increasingly challenged South American supply streams and higher demand pressures.”

Wood Mackenzie is forecasting major deficits in copper to 2030, attributed largely to unrest in Peru and higher demand for copper in the energy transition industry.

The South American country, which accounts for 10% of world copper supply, has been racked by protests since its former president, Pedro Castillo, was ousted last December.

In January Glencore suspended operations at its Antapaccay copper mine, after protesters looted and set fire to its premises.

A strike is currently underway at the Las Bambas mine owned by China’s MMG Ltd., with the union reportedly considering an indefinite strike from Nov. 28 if the company does not meet its demands.

Next door in Chile, the largest red-metal producer, accounting for 27% of global supply, recorded a y/y decline of 7% last November.

“Overall we believe Chile will likely produce less copper from 2023 to 2025,” Goldman Sachs wrote in a note dated Jan 16.

The Cobre Panama mine has been enduring a blockade of supplies and owner First Quantum Minerals warned on Monday it would have to suspend operations if the ongoing port blockade continues.

In a background to the controversy, Mining.com noted the Vancouver-based firm and the government of Panama last month reached a multi-billion-dollar agreement that ended months of negotiations between the two parties. The forthcoming legislation triggered a series of violent protests that almost paralyzed Panama City. Demonstrators claim the new contract was fast-tracked with little transparency and accused the government of corruption. Locals are also worried about the mine’s effects on drinking water and the Panama Canal.

As for the green energy transition, Wood Mackenzie analysts estimate a 6-million-ton shortfall by next decade, meaning 6 Escondida’s would need to come online within that period – this is 100% NOT going to happen, not even close.

The problem is there aren’t enough new mines, let alone large ones. Bloomberg NEF estimates refined copper demand will grow by 53% by 2040 but supply will increase only 16%.

A report by another consultancy, McKinsey, found that electrification is projected to increase annual copper demand to 36.6 million tonnes by 2031, with supply projections offering a pathway to 30.1Mt, leaving 6.5Mt of capacity to be found.

Jerome Leroy, vice-president of the Canadian business unit of cable supplier Nexans, pointed to forecasts suggesting production capacity will grow to 27 million tonnes a year by the end of this decade, whereas demand could rise as high as 35 million tonnes. He warned a shortfall could materialize as early as next year.

Why can’t more copper be mined? The International Copper Study Group says that since 1960, there have always been, on average, 38 years of reserves in the ground. In fact, despite increased demand for copper, reserves have grown (as copper prices rise uneconomic ore becomes economic), and there is more identified copper available than at any other time in history, the group asserts.

Moreover, the US Geological Survey estimates that, while the world has produced 700 million tonnes of copper, there are 2.1 billion tonnes worth of discovered copper deposits yet to be tapped.

Two reasons we aren’t extracting more copper are costs (incentive pricing in the copper industry is considered to be US$11,000t) and regulatory delays.

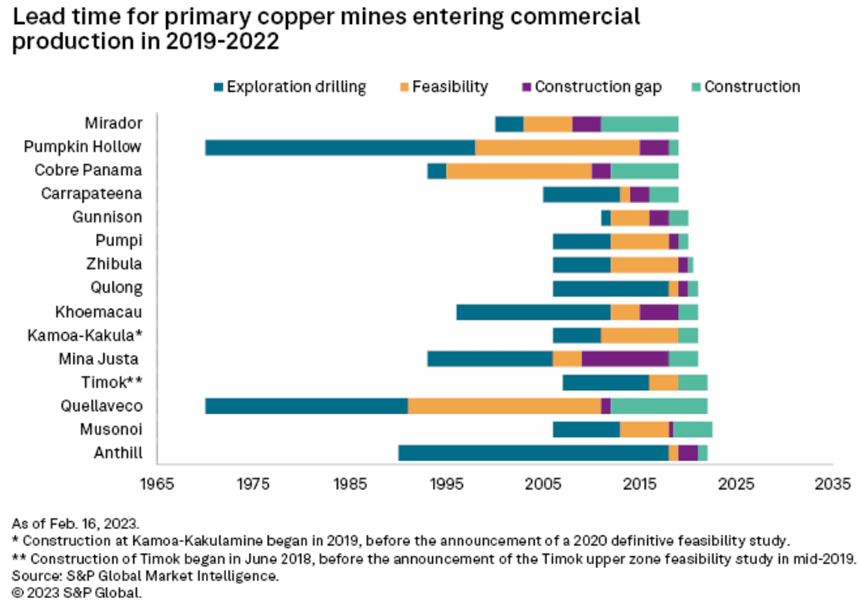

According to a recent blog post by copper wire manufacturer Kris-Tech, determining whether a site has enough copper ore to make the investment worthwhile can take two to eight years, and another four to 12 years before it can start operations. In North America, it can take up to 20 years for a mine to go from discovery to production.

“New primary copper mines starting up between 2019 and 2022 had an average lead time of 23 years from discovery to commercial production.”

“New copper projects expected to enter commercial production in 2023 include Quebrada Blanca Phase 2 in Chile, Kisanfu in DRC, Kalongwe in DRC, Tshukudu in Botswana, Anthill in Australia, Serrote in Brazil and Udokan in Russia, potentially adding around 550,000 metric tons of copper production in 2023. The bulk of future copper supply growth will come from planned expansions at current mines, however, rather than the development of new operations.” S&P Global Commodity Insights

Current mines, meanwhile, are facing dwindling supplies of easy to access copper ore, meaning miners must dig deeper; the increased excavation obviously costs more.

I get that exploration isn’t easy, especially, imo, given that most of the world’s big, high-grade deposits have already been found. But why can’t the large copper miners simply tap into their existing reserves to meet growing demand?

The truth is, they have been. Instead of sending exploration teams around the world turning over rocks to find the next gigantic copper deposit, the main way copper companies have added reserves is by lowering their cut-off grades.

The way this is done is fairly simple. A mine plan is based on the “cut-off grade”, which is the minimum grade needed to make a unit of rock economic to extract at a given price. Any ore below this grade stays in the ground. When metal prices rise, the mining company makes more per tonne, so it is able to “lower the cut-off grade” and still make a profit. It’s essentially turning what was previously waste rock at old pricing into mineable ore at the new prices.

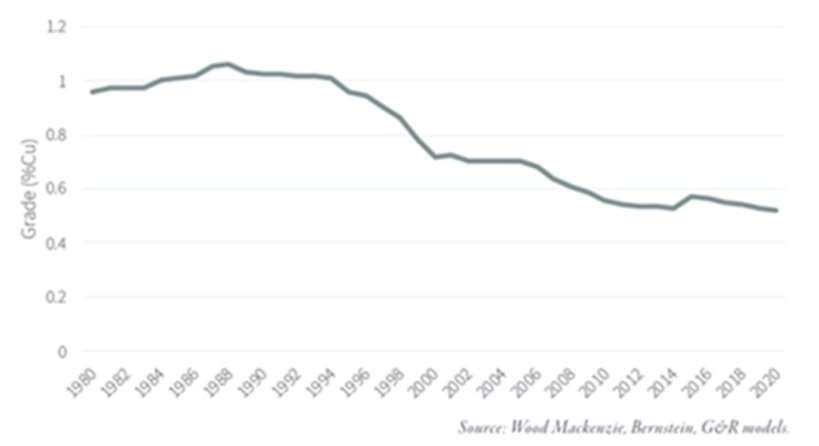

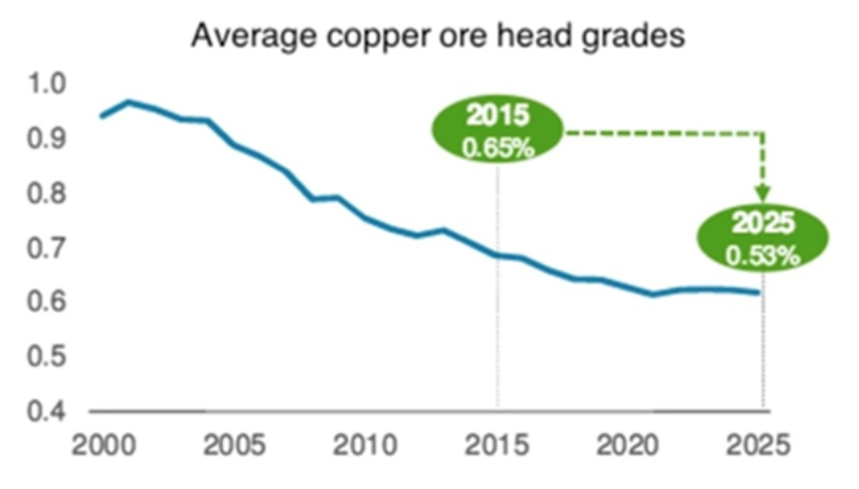

By 2015, the industry’s head grade was already 30% lower than in 2001, and the capital cost per tonne of annual production had surged four-fold during that time — both classic signs of depletion.

According to the Goehring & Rozencwajg the industry is “approaching the lower limits of cut-off grades and brownfield expansions are no longer a viable solution. If this is correct, then we are rapidly approaching the point where reserves cannot be grown at all.”

The importance of making new discoveries in establishing a sustainable copper supply chain is obvious.

Over the past 10 years, greenfield additions to copper reserves have slowed dramatically, with tonnage from new discoveries falling by 80% since 2010.

Average grade of remaining copper reserves

Several large copper mines have mined out all the ore in open pits and are heading underground for the higher-grade, but more expensive to extract material. One example is Oyu Tolgoi in Mongolia, which began underground operations in May.

An article in Japan Times states that, As demand for copper surges, supply is increasingly likely to come from mines like this one on the arid steppe: expensive, technically complex, outside traditional copper jurisdictions and operating under the eye of governments jealously guarding their natural resources.

“There’s a huge crisis,” says Doug Kirwin, one of the earliest geologists to work at the deposit that became Oyu Tolgoi, or Turquoise Hill, named after the area’s rocks, stained by oxidized copper.

“There’s no way we can supply the amount of copper in the next 10 years to drive the energy transition and carbon zero. It’s not going to happen,” adds Kirwin, now an independent consulting geologist. “There’s just not enough copper deposits being found or developed.”

The article notes the looming copper shortfall has encouraged copper mergers and acquisitions (M&A), such as Glencore’s attempted hostile takeover of Teck Resources, Newmont’s bid for Australia’s Newcrest, and BHP’s acquisition of copper producer Oz Minerals.

The most recent copper deal saw China’s MMG agreeing to pay $1.9 billion for Cuprous Capital, a private company that owns the Khoemacau operation in Botswana.

However, Japan Times concludes that none of these deals, which simply transfer copper reserves from one company to another, will alter the global copper balance, given that “building new mines, as opposed to buying them, is still too much of a headache,” and that exploration spending remains far short of what is required.

According to Goldman Sachs regulatory approval for new copper mines has fallen to the lowest in a decade, an ominous sign of things to come as regulatory approval to build a mine can take up to 20 years..

“Mines are getting older, mines are getting deeper, and mines are getting lower grade,” the news site quotes David Radclyffe, managing director at Global Mining Research. “Then you’ve had the added complications of the need to conform with the shift in terms of environmental requirements. And political risk on top of that.”

“Capital spending by mining companies is set to decrease 11% in 2023, with exploration spending likely to fall by 10%-20%.” S&P Global Commodity Insights’ principal metals and mining analyst Kevin Murphy.

Asian offtakes

Another obstacle to addressing the copper deficit is the fact that four of the five new large mines have offtake agreements already in place.

At Cobre Panana, nearly half of the 300,000 tonnes per year (tpy) production goes to Korea. Under a 15-year offtake agreement, Canadian miner First Quantum Minerals will ship 122,000 tpy of copper concentrates from Cobre Panama to South Korean copper smelter LS Nikko.

The largest, by far, of the 5 mines expected to deliver 80% of new copper production is Robert Friedlands Kamoa-Kakula copper project in the Democratic Republic of Congo (DRC). The project is a joint venture between Ivanhoe Mines (39.6%), Zijin Mining Group (39.6%), Crystal River Global Limited (0.8%) and the DRC government. Kakula reached commercial production on May 25, 2021, and while output is set for 200,000 tpy in Phase 1, a second phase would add 200,000 tpy and peak production would exceed 800,000 tpy.

(Remember, the prediction is we need a million tonnes of new copper production PER YEAR for 6 years. Kamoa-Kakuls’s future production of 800,000tpy almost fills one year of the 6. Where are the other 5 years of new 1m tpy coming from?)

Ivanhoe signed two offtake deals, one with a subsidiary of its partner firm, China’s Zijin Mining; the other with Chinese commodities trader CITIC Metal, to sell each 50% of the copper production from Kakula — the first of two mines involved in the joint venture. In other words, 100% of Kamoa-Kakula’s Phase 1 production goes to China.

That leaves three mines in Chile — Escondida, Spence and Quebrada Blanca’s “QB2” expansion. In 2016 BHP, the majority owner of Chile’s Escondida, the largest copper mine in the world, committed to spend just under $200 million to expand its Los Colorados concentrator. The expansion would help offset declining ore grades and add incremental copper production to reach an average 1.2 million tonnes a year over the next decade. BHP owns a 57.5% share in Escondida, Rio Tinto owns 30%, and the remaining 12.5% is owned by JECO Corp and JECO2 Ltd.

JECO is a Japanese joint venture between Mitsubishi Nippon Mining & Metals and Mitsubishi Materials Corp. It is not immediately clear whether any of Escondida’s production is bought by JECO Corp.

BHP said once the Spence mine expansion hits full production, it would produce 300,000 tpy until at least 2026. Spence ownership is split 50-50 between BHP and Santiago-based Minera Spence SA.

Teck Resources’ Quebrada Blanca Phase 2 project is expected to produce 316,000 tpy of copper equivalent for the first five years of its 28-year mine life. In 2019 the Canadian company closed a $1.2 billion transaction whereby Tokyo-based Sumitomo Metal Mining and Sumitomo Corp will, through an $800 million and a $400 million contribution, acquire a 30% interest in project owner Compañia Minera Teck Quebrada Blanca S.A. (“QBSA”). Like Escondida, it is unclear whether the two Japanese companies will take a portion of QB2’s production, or whether they will simply share in the profits.

Summing up, our analysis shows that in four of the five mines where new copper supply is concentrated, there are offtake agreements either in place or implied, with non-Western buyers. In the case of Kamoa-Kaukula, 100% of initial production will be split between two Chinese companies, one of which owns 39.6% of the joint venture project. Nearly half of Cobre Panama’s annual production goes to a Korean smelter under a 2017 offtake agreement. Escondida and Quebrada Blanca are both partially owned by Japanese companies — one can assume that a corresponding percentage of production will be going there.

World Copper Factbook 2020

Analysts do not concern themselves with ‘who’ owns the copper, their only concern is with the amount of global supply. Unfortunately where its going – mostly China, S.Korea and Japan – means its hardly global supply. Fact is, the west, that’s us, has almost no off-take agreements in place for 80% of the worlds future copper supply.

Commodity analysts like to talk about the wave of global supply about to crash onto the copper market, but they don’t seem to realize that 80% of the foreseeable copper supply is coming from just five mines, but four out of five have offtake agreements with non-Western buyers.

That supply is locked up. It’s been previously stated that we need to find 6 million more tonnes of copper, 1 million per year of new copper production if we want to alleviate the deficit — the equivalent production of one Escondida mine each year — but only one of the five mines, Kamoa, has the capability of producing close to that much copper. But Kamoa’s production is going to China.

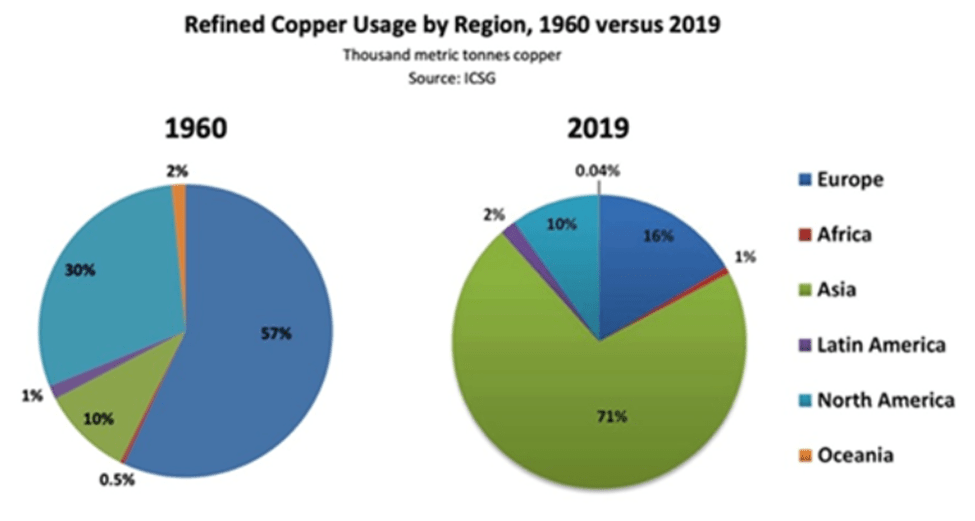

At AOTH we make a clear distinction between global copper supply and the global copper market. Mined copper that is locked up by offtake agreements should not rightly be lumped in with global supply, because it will never reach the United States, Canada or Europe. Instead, this copper will go straight to smelters in China for use in Chinese industry, to South Korean smelters for South Korean industry, and to Japanese smelters for Japanese industry.

We know that Chile, the world’s biggest copper producer, has problems with water and is having to desalinate seawater used for mining copper in the country’s arid north. Cochilco, the country’s copper commission, estimates the use of desalination by mining to increase 156% through 2030, with 90% of the desalinated seawater used for copper processing.

Reuters said that severe droughts are drying up rivers and reservoirs vital for production of zero-emission hydropower in several countries.

As global warming makes already scarce water and mineral resources more difficult and expensive to access, the protection of existing mines and the hunt for new deposits will intensify, resulting in potentially lower production, higher operating costs and conflicts between both water and land users.

With much of the world currently experiencing droughts, and the effects of warming occurring more frequently and powerfully, it seems to me that there’s a very real risk to future metals output.

“Disruptions at copper mines caused by extreme weather and labour issues, for example, are predicted to worsen, likely affecting a record 1.6 million tonnes of production this year, Goldman Sachs analysts say, a headache for companies hunting for minerals to power the green energy boom as their deposits get depleted.” Reuters

It’s going to be hard enough to maintain the current 22Mt of mined copper production let alone doubling it. Remember, over 200 copper mines are expected to run out of ore before 2035, 80% of new production is in just 5 mines, with the majority of that ore locked up in off-take agreements with Asian buyers.

Beyond electrification and decarbonization, we will still need enough copper for all its other uses, in construction wiring & plumbing, infrastructure build outs, transmission lines, etc. On top of this there is the surging need for copper in developing countries, whose populations want to “live like an American.”

“The average American will consume 53 times more goods and services than someone from China….With less than 5 percent of world population, the U.S. uses one-third of the world’s paper, a quarter of the world’s oil, 23 percent of the coal, 27 percent of the aluminum, and 19 percent of the copper.” Sept 2012, Sierra Club’s Dave Tilford

Conclusion

Asian countries are switching to ore imports as they expand refinery/ smelting capability. This does not bode well for Western copper supplies. Remember, for the foreseeable future, copper supply is 80% concentrated in just five mines, all of which have major off-take agreements with South Korea, Japan or China. For instance, 100% of the massive Kamoa mine’s off-take will go to China.

The CRU anticipates a 5% growth in copper demand in China this year, while Goldman Sachs Group Inc. has designated copper as one of its top commodity picks for the next year, citing a “robust green demand environment,” particularly in China.

According to natural resources investment firm Goehring & Rozencwajg;

“Driven by concerns of an impending global recession, copper sentiment remained bearish during the second quarter. On the other hand, copper’s short-term fundamentals became increasingly bullish. Mine supply disappointed again in the first four months of 2023, according to the World Bureau of Metal Statistics (WBMS).

Chilean production continues to be particularly problematic. For the first four months of the year, Chilean mine supply fell by nearly 2% compared to last year. Codelco warned that production could hit the lowest level in twenty-five years. In June, André Sougarret abruptly resigned as Codelco’s Chief Executive Officer after only one year on the job. Mr. Sougarret cited the numerous “complexities” facing the Chilean copper mines.

Chile supplies almost one-quarter of all copper production and, in past letters, we have discussed the issues plaguing their copper industry; in particular, declining ore grades, water shortages, labor issues, and uncertain fiscal regimes all negatively impacted production. Unfortunately, we do not expect any of these issues to improve going forward. Global copper mine supply contracted by 0.2% in the first four months of 2023 compared to last year, driven by disappointments in Chile.

Meanwhile, global copper demand remained robust in both OECD and non-OECD countries. For the first four months of 2023, OECD copper demand increased by a robust 3.7%. Despite countless bearish articles in the financial press, Chinese copper demand continues to surge, with refined demand rising by 8% year-on-year.” An excerpt from its Q2 2023 commentary.

China is already gobbling up copper and copper ore at an incredible rate, and now they want even more. I have no doubt China is delibertaly tightening their grip on the global copper market like they have already accomplished in the lithium, cobalt, graphite, nickel, steel and rare earths supply chains.

“In its critical minerals strategy in December, Canada listed copper as one of the top six critical minerals, along with lithium, graphite, nickel, cobalt and rare earth elements, due to its importance in the clean technology sector.” Financial Post

It appears the West has been snookered again.

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

Namibia Critical Metals Inc. (TSX-V: NMI) (OTCQB: NMREF) is pleased to announce that Japan Organizat... READ MORE

Eldorado Gold Corporation (TSX: ELD) (NYSE: EGO) today reports the Company’s financial and operati... READ MORE

DPM Metals Inc. (TSX: DPM) (ASX: DPM) announced its operating and financial results for the second q... READ MORE

IMC Rare Earths Ltd, a company focused on the mineral exploration and development of magnet rare ear... READ MORE

Fairchild Gold Corp. (TSX-V: FAIR), is pleased to announce the closing, on July 29, 2026, of its pre... READ MORE