Minera Alamos Inc. (TSX-V: MAI) is pleased to announce the positive results of an independent Preliminary Economic Assessment for its La Fortuna Project in Durango, Mexico. The PEA was prepared in accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects by CSA Global Geosciences Canada Ltd of Toronto, Canada. (Note to reader: Unless stated all currency references are in US dollars).

Table 1 – PEA Summary

| US$ | CDN$ | |

| Pre-Tax NPV (7.5%) | $103,800,000 | $134,800,000 |

| Pre-Tax IRR | 122% | 122% |

| After-Tax NPV (7.5%) | $69,800,000 | $90,600,000 |

| After-Tax IRR | 93% | 93% |

| Pre-Tax Payback Period | 9 months | |

| After-Tax Payback Period | 11 months | |

| Average Annual Production | 43,000 oz Gold, 220,000 oz Silver, 1,000 t Copper (50koz GEO1) | |

| Preproduction Capital | $26,900,000 | $34,900,000 |

| LOM Average AISC 2 | $440/oz | $571/oz |

| Mine Life | 5 years | |

| Mill Throughput (avg. tpd) | 1,100 | |

| Mill Grade & Recovery | 3.68 g/t Au (90% recovery) | |

| Gold Price | $1,250/oz | |

| Silver Price | $16/oz | |

| Copper Price | $5,725/tonne | |

| FX Rate (CDN$/US$) | 0.77 | |

| Notes: | ||

| 1. | GEO – Gold Equivalent Ounces | |

| 2. | “AISC per ounce” is a non-GAAP financial performance measures with no standardized definition under IFRS; additional reference info at bottom of release | |

| 3. | Base case prices for gold, silver and copper were assessed at values approximately 2%-7% below the three-year trailing average prices for each of the metals and below the majority of the publicly available forward looking estimates available as of July 2018 | |

PEA Cautionary Note:

Readers are cautioned that the PEA is preliminary in nature and there is no certainty that the PEA results will be realized. Mineral resources are not mineral reserves and do not have demonstrated economic viability. Additional work is needed to upgrade these mineral resources to mineral reserves.

“With an after-tax Internal Rate of Return in excess of 90%, today’s excellent PEA results confirm that the La Fortuna Project provides a robust base for the next phase of gold production in the Company’s growth pipeline,” commented Darren Koningen, Chief Executive Officer. “The simplified gold recovery process outlined in the study represents a conservative starting point that is well suited to the initial project resource which, to date, has been based exclusively on previously drilled mineralization. As our engineering work progresses we continue to find opportunities to reduce the initial project capital requirements and improve overall project economics. Coupled with our strategic partnership with Osisko Gold Royalties that includes an option to provide a significant portion of the project capital requirements in return for a Project royalty, these additional optimizations will greatly reduce the upfront funding requirements of this already low capital cost operation.”

“This PEA represents a key milestone for the Company as we begin to deliver to the market’s attention the underlying project economics of our development pipeline that focuses on cost-efficient and targeted production that can incrementally build a significant production profile over time,” commented Doug Ramshaw, President. “With the recently submitted commercial permit applications at the Santana project and ongoing work at the Company’s Guadalupe de los Reyes project we are aggressively expanding our activities on multiple fronts. We continue to envision a plan whereby targeted production from the development of the Santana project will support the modest capital requirements of the La Fortuna operation.”

Production and Economic Highlights

Table 2 – Overview of PEA Results and Assumptions

| Unit | Base Case | ||

| Inputs | Gold Price | $/oz | $1,250 |

| Silver Price | $/oz | $16 | |

| Copper Price | $/t | $5,725 | |

| Exchange Rate | MXP/USD | 19 | |

| Economics | Net Cash Flows (Undiscounted) | $ | $141,000,000 |

| Pre-Tax | NPV at 7.5% | $ | $104,000,000 |

| IRR | % | 122% | |

| Payback Period | Months | 9 | |

| Economics | Net Cash Flows (Undiscounted) | $ | $96,000,000 |

| Post-Tax | NPV at 7.5% | $ | $70,000,000 |

| IRR | % | 93% | |

| Payback Period | Months | 11 | |

|

NPV Discount Rate Sensitivities |

|||

| Pre-Tax | Net Cash Flows (Undiscounted) | $ | $141,000,000 |

| NPV at 5% | $ | $114,000,000 | |

| NPV at 10% | $ | $94,000,000 | |

| Post-Tax | Net Cash Flows (Undiscounted) | $ | $96,000,000 |

| NPV at 5% | $ | $77,000,000 | |

| NPV at 10% | $ | $63,000,000 | |

Capital & Operating Cost Estimates

Table 3 – Initial and Sustaining Capital Costs

| Area | Initial ($000) | Sustaining ($000) | Total ($000) |

| Mining (contractor mobilizations) | $1,000 | $1,000 | |

| Site Development/Infrastructure | $3,500 | $3,500 | |

| Mineral Processing | $15,000 | $7,100 | $22,100 |

| Tailings Management | $2,000 | $2,000 | |

| Closure | $3,000 | $3,000 | |

| Salvage Value | ($3,000) | ($3,000) | |

| Contingencies (incl. owner’s costs) | $5,400 | $5,400 | |

| TOTAL PROJECT | $26,900 | $7,100 | $34,000 |

| *Note: Start-up working capital to be provided by concentrate purchasers on credit revolver basis. | |||

Table 4 – Operating Costs (OPEX)

| Area | $/tonne Mineralized Material*2 |

$/unit | |

| Open Pit Mining | $11.80 | $2.15 | per tonne mined |

| Processing | $15.95 | $22.89 | per tonne milled |

| Stockpile/Ore Sorting*1 | $1.73 | $4.00 | per tonne sorted |

| G&A | $3.86 | $5.54 | per tonne milled |

| All-In OPEX | $33.34 | ||

| Notes: | |||

| 1. | “Ore Sorting” as used in the context of Table 4 is a commercial term referring to sensor-based rock sorting technology and is not related to project resources/reserves. Ore sorting equipment is implemented in Year 3 for upgrading of mid-grade stockpiles | ||

| 2. | “Mineralized Material” represents mined material in excess of 0.8 g/t Au cut-off (includes direct milling material + stockpiled material to be upgraded via ore sorting prior to milling) | ||

Mineral Resources

This PEA is based on a new mineral resource estimate prepared for the La Fortuna project by Scott Zelligan, P.Geo., as part of the current report. The mineral resource estimate is based on the results from 125 core drill holes completed to date on the project. Wireframes were prepared using the drill hole information combined with geological interpretations of the deposit and validated through observations and sampling of accessible historical underground openings. Further details related to the current mineral resource estimate are presented in a later section. The table below outlines the total base case Mineral Resources, including those that were not included as part of the PEA mine plan.

Table 5 – Mineral Resource Estimates (1.0 g/t Au cutoff grade)

| Resource Category | Au (g/t)

Cut-off |

Tonnes (t) | Au (g/t) | Ag (g/t) | Cu (%) | Au oz |

Ag oz |

Cu t |

| Measured | 1.0 | 1,755,400 | 2.96 | 17.5 | 0.23 | 167,100 | 987,800 | 4,000 |

| 1.5 | 1,309,700 | 3.55 | 19.5 | 0.25 | ||||

| 2.0 | 1,012,100 | 4.09 | 21.0 | 0.28 | ||||

| 2.5 | 795,300 | 4.59 | 22.4 | 0.30 | ||||

| 3.0 | 639,400 | 5.04 | 23.5 | 0.32 | ||||

| Indicated | 1.0 | 1,714,300 | 2.59 | 15.5 | 0.21 | 142,800 | 854,400 | 3,600 |

| 1.5 | 1,241,400 | 3.11 | 17.5 | 0.24 | ||||

| 2.0 | 886,400 | 3.65 | 19.2 | 0.27 | ||||

| 2.5 | 626,600 | 4.24 | 21.0 | 0.30 | ||||

| 3.0 | 458,500 | 4.80 | 22.2 | 0.32 | ||||

| Measured + Indicated | 1.0 | 3,469,700 | 2.78 | 16.5 | 0.22 | 309,800 | 1,842,200 | 7,600 |

| 1.5 | 2,551,100 | 3.34 | 18.5 | 0.24 | ||||

| 2.0 | 1,898,500 | 3.88 | 20.2 | 0.27 | ||||

| 2.5 | 1,421,900 | 4.44 | 21.8 | 0.30 | ||||

| 3.0 | 1,097,900 | 4.94 | 23.0 | 0.32 | ||||

| Inferred | 1.0 | 156,300 | 1.72 | 8.5 | 0.09 | 8,600 | 42,700 | 100 |

| 1.5 | 78,612 | 2.21 | 9.2 | 0.10 | ||||

| 2.0 | 38,059 | 2.73t | 11.1 | 0.12 | ||||

| 2.5 | 18,169 | 3.28 | 13.1 | 0.14 | ||||

| 3.0 | 7,589 | 4.04 | 15.6 | 0.18 | ||||

| Notes: | ||||||||

| 1. | The effective date for this mineral resource estimate for La Fortuna project is July 13, 2018. All material tonnes and metal values are undiluted. | |||||||

| 2. | Mineral Resources are calculated assuming a cut-off grade of 1.0 g/t Au, which is considered reasonable and consistent for this type of deposit with open pit mining methods. | |||||||

| 3. | Mineral resources which are not mineral reserves do not have demonstrated economic viability. The estimate of mineral resources may be materially affected by environmental, permitting, legal, title, socio-political, marketing, or other relevant issues. | |||||||

| 4. | The mineral resources presented here were estimated using a block model with a parent block size of 5 m by 5 m by 5 m sub-blocked to a minimum block size of 0.6 m by 0.6 m by 0.6 m using ID3 methods for grade estimation as this method best represented the grade distribution in the sample data. | |||||||

| 5. | Due to the geometry of the deposit and the nature of the grade distribution, the estimation was divided between the upper and lower portions of the mineralized volume with search parameters optimized for each portion. | |||||||

| 6. | Individual composite assays were capped at the following values according to histogram/probability and decile analyses – 30 g/t gold, 60 g/t silver, 1% copper | |||||||

| 7. | A density of 2.65 t/m3 was chosen for the tonnage estimate. Data available from dry bulk density studies indicated an average density of 2.72 t/m3 for mineralized material, while the quartz monzonite material had an average density of 2.61 t/m3. The value of 2.65 was chosen by averaging the two then rounding down to the nearest 0.05 interval to be conservative | |||||||

| 8. | The mineral resources presented here were estimated using the Canadian Institute of Mining, Metallurgy and Petroleum (CIM), CIM Standards on Mineral Resources and Reserves, Definitions and Guidelines prepared by the CIM Standing Committee on Reserve Definitions and adopted by CIM Council May 10, 2014. | |||||||

| 9. | The mineral resource estimate was prepared by Scott Zelligan, B.Sc., P.Geo., and independent resource geologist of Coldwater, Ontario. | |||||||

| 10. | Gold price is US$1,250/ounce, silver price is US$16/ounce, and copper price is US$5,725/tonne. | |||||||

| 11. | The number of metric tonnes is rounded to the nearest hundred. Any discrepancies in the totals are due to rounding effects. | |||||||

Mining

The mineralization at the Project extends close to surface and is amenable to conventional open pit mining methods utilizing front-end loaders and trucks. Using a preliminary Whittle pit shell for the deposit ($1,250/oz gold, $2.50/t mining, $30.00/t processing, 95% recovery, 45-degree pit slopes) as a guide a full open pit mine plan was completed. LOM mineralized material was separated in grade baskets (+0.8, 1.2, 1.6, 2.0 g/t Au) so that a more complete engineering cost evaluation could be completed and used as the basis of a final five-year production plan for the project. Mineralized material was grouped as Direct Milling (>1.6 g/t Au) and Mid-Grade (0.8 – 1.6 g/t Au) which is to be stockpiled and upgraded via ore sorting prior to milling (starting Year 3). No inferred resources were utilized in the PEA mine planning and further optimization efforts aimed at cut-off grades and the smoothing of waste mining activities may provide additional economic upside for the project.

Table 6 – Fortuna Processing Plant Mill Feed Schedule (diluted)

Year |

Total Mill Feed (tonnes) |

Au (g/t) |

Ag (g/t) |

Cu (%) |

Gold (ounces) |

Total Mined Material (tonnes) |

|

| 1 | 380,000 | 3.86 | 21.24 | 0.29 | 47,200 | 2,814,400 | |

| 2 | 380,000 | 3.91 | 20.27 | 0.27 | 47,800 | 2,848,200 | |

| 3 | 410,000 | 3.39 | 21.85 | 0.28 | 44,700 | 2,335,700 | |

| 4 | 410,000 | 3.47 | 19.98 | 0.29 | 45,800 | 4,637,200 | |

| 5 | 418,400 | 3.78 | 16.79 | 0.22 | 50,900 | 3,095,700 | |

| 1,998,400 | 3.68 | 19.96 | 0.27 | 236,600 | 15,731,200 | ||

| Notes: | |||||||

| 1. | Mill Feed totals include direct milling material (1,626,000 tonnes) and mid-grade stockpiled material upgraded starting in Year 3 via crushed ore sorting (372,400 tonnes). | ||||||

| 2. | Mine dilution applied as follows – 10% for direct milling material (dilution grade equivalent to average grade of next lower mine grade basket) and 25% for low-grade material to stockpile (0.5 g/t Au dilution grade | ||||||

| 3. | Total mined material values include all production from open pit mine (mineralization + waste) for noted intervals. | ||||||

Pit bench heights were selected at 5m intervals in order to provide good ore/waste selectivity although use of larger bench heights in zones of primarily waste should be considered as part of future optimization studies. Overall average pit slopes with the benches/ramps in place are approximately 43 degrees for three sides and 41 degrees overall for the north wall. Rock competency is reasonable and higher pit slopes may be considered once the appropriate geotechnical information is available. Mineralized and waste materials are hauled using 25t trucks approximately 500m (maximum) to the waste dumps/mineral stockpile locations near the mine. Crushed stockpile material is then transported to the plant processing facilities located at a distance less than 1.5km.

All drilling/mining/crushing operations at the Project will be accomplished via an open pit mining contractor. Mining costs were developed for the project from first principals utilizing recent Mexican cost information. Contractor availability in northern Mexico is currently high and rates are competitive. An appropriate profit factor was applied to the calculated owner operator rates and the values were benchmarked against recent operational experience by Minera Alamos mining personnel. An additional factor was applied to account for the fact that the project is located a few hours from a major population base. Mine planning and supervision activities will be performed by Minera Alamos personnel and these costs are excluded from contractor rates.

Processing

A simplified base case process was utilized for the La Fortuna plant site. Mineralized material from the mine is stockpiled and crushed to a size of <3/4″ prior to being transported to the process plant. The overall processing facilities consist of a primary coarse grind to 80% passing 250-300 microns followed by a bulk sulphide concentrate flotation. Bulk concentrate is reground (80 microns) prior to a final flotation producing a copper concentrate. Centrifugal gravity gold recovery circuits are included in both the primary and concentrate reground circuits to extract free gold as a concentrate. Tailings from the flotation circuit are dewatered via filtration and dry-stacked in the tailings containment area adjacent to the processing plant.

Overall gold recovery for the PEA study has been conservatively estimated at 90%. No final gold refining facilities are to be constructed at the Fortuna site although this decision can be revisited in the future should site production rates increase. Approximately half of the gold is extracted as a gravity concentrate which will be cyanide leached at site and loaded onto activated carbon for shipping outside of Mexico for final doré production. The other half of the recovered gold reports to the copper flotation concentrate (along with the majority of the copper and silver) which is filtered and transported to the port facilities at Guaymas (approximately 500 km) for final sale.

The Company has purchased a used 2000 tpd processing facility (grinding/flotation/filtration) that has been used as the basis for the Fortuna project processing facilities. The size of the major equipment items allows for plant throughput to be increased from the currently assumed 1100 tpd rate as the size of the project resource increases.

DEXTR (x-ray) ore sorting has been included in the overall project plans as a method to upgrade mid-grade (0.8-2.0 g/t Au) mineralized material from the mine (and future potential project resources). Testwork has demonstrated that sorting of this material at normal project crush sizes can recover +80% of the contained gold into a sorted concentrate with gold contents similar to the high grade (3.5 – 4.0 g/t Au) direct milling material from the mine. It is conservatively assumed that an ore sorting machine will be purchased and installed in Year 3 of mining operations to upgrade this material. In the current operations plan only 20% of the LOM contained gold ounces sent to the processing plant have been upgraded in this manner.

Table 7 – Summary of La Fortuna Metallurgical Results

| Product | Grade | Metal Recoveries (%) | ||||

| Au (g/t) | Silver (g/t) | Copper (%) | Au | Silver | Copper | |

| Mill Feed (LOM) | 3.68 | 20 | 0.27 | |||

| Products | ||||||

| Gravity Concentrate*1 | N/A | 45 | ||||

| Copper Flotation Concentrate | 120 | 1250 | 18 | 45 | 85 | 90 |

| *1Gravity concentrate is leached in cyanide and adsorbed onto activated carbon for shipping offsite for final processing. For PEA modelling purposes it was assumed that gold was the only material payable metal recovered by gravity | ||||||

Infrastructure

Access

The La Fortuna project is accessible by road from Culiacan (Sinaloa state capital – population approx. 1MM), a driving distance of approximately 85 kilometers. At present the road is paved to within approximately 30 km of the town El Barco which is situated at the river immediately south of the project area. The remaining road is graveled, graded and of reasonable width for much of the route. It has been anticipated that some relatively minor upgrading of portions of this road (primarily in areas with a sharp turning radius) will be required in order to improve access for larger trucks to reach the Fortuna project area.

Preliminary engineering has been completed to locate new access roads within the project area required for start of the La Fortuna operations. This includes a total of approximately 5 km of gravel surface suitable for the operation of mining trucks.

Power

The closest small villages to the Project site (El Barco and San Fernando) have less than 100 inhabitants and are currently not serviced via the national power grid. Grid power is being extended along the state highway from Culiacan as it is widened and paved (currently within 30km of the project) but it is unknown when it will ultimately be available and what load capacity would exist.

It is assumed for the foreseeable future that all power required for the Project will be generated at site via diesel generators. The total operating plant power load is estimated at approximately 2MW which will be supplied via multiple generator units (operating + standby) to build in redundancy for maintenance, etc. Primary generators are to be located within close proximity to the processing plant area so site power line requirements will be negligible. Wherever possible, large power consumers not associated with the processing plant (i.e. portable crushers) are self-contained with local diesel hydraulic/electric generation. Small auxiliary generators will be utilized as necessary for minor requirements (i.e. plant camp/offices).

At current fuel prices in Mexico power generation via diesel equipment is equivalent to an electric power cost of $0.25-0.30/kWh which has been used for budgeting. Should grid power eventually arrive at the project area, power costs for the project would be reduced by 50% or more.

Water Management

The Humaya river flows roughly northwest-southeast approximately 500m from the planned La Fortuna processing plant area. This river has a year-round supply of flowing surface water and discussions with the relevant permitting authorities have indicated that the project would be permitted to extract river water directly for process uses. In addition, a seasonal creek bed that runs east-west and connects with the Humaya river is located a few hundred meters south of the plant site. Hydrogeological studies are underway to establish optimal sources of groundwater that would also be suitable for the project’s requirements.

Based on local observations, it is expected that river/ground water levels occur at the 250-300m elevation (above sea level). Water would be pumped from this elevation the short distance to the plant site which is located just above 500m (above sea level). Process water removed from the plant filtered tailings will be recycled as much as possible in order to minimize fresh process water make-up requirements.

Permitting Status

The Environmental Impact Assessment (EIA) for mining projects in Mexico starts with an application for the following primary permitting documents:

Following the completion of the EIA process a number of other registrations and local/state permits are required before the start of commercial production. Important among these are water rights through the Comisión de Agua (National Water Commission or CONAGUA), permits for the storage and use of explosives as well as construction permits from the local municipality.

The MIA-ETJ permit applications were submitted by Minera Alamos for the La Fortuna project in 2018 and are pending. The submitted permitting documents included an expanded scope of processing facilities that included additional stages not required for the current start-up plan (i.e. concentrate cyanidation and detoxification). This provides the company with added flexibility in the future to modify the existing operation in order to accommodate new potential regional sources of mineralization.

The Company does not currently own any surface rights in the La Fortuna area. The surface rights over the area are held jointly by the residents of the Tabahueto ejido (a Mexican agricultural cooperative). In 2016 the Company started the discussions with the local ejido regarding the necessary surface rights for the development of the La Fortuna project. On February 16th, 2017 at a general meeting the community voted unanimously to enter into a 25-year agreement to rent 235 Ha of surface area required by the Company (agreement signed formally in June 2017).

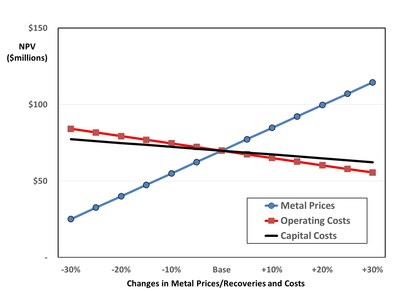

Sensitivity Analysis

Table 8 – Sensitivity Analysis (7.5% discount / after-tax)

| NPV ($million) | Input Factor | ||||||

| Input | -30% | -20% | -10% | Base | +10% | +20% | +30% |

| Metal Prices/Recovery | 25.1 | 40.0 | 54.9 | 69.8 | 84.7 | 99.6 | 114.5 |

| OPEX | 84.1 | 79.3 | 74.6 | 69.8 | 65.0 | 60.3 | 55.5 |

| CAPEX | 77.3 | 74.8 | 72.3 | 69.8 | 67.3 | 64.8 | 62.3 |

Project Opportunities

The PEA identifies several project opportunities to further enhance project economics. These include:

Qualified Person Statements

The 2018 PEA was prepared and led by CSA Global Geosciences Canada Ltd., in collaboration with other consultants, all Qualified Persons (“QPs”) as defined under Canadian National Instrument 43-101. The QPs have reviewed and approved the content of this news release. All of the QPs are “independent” of the Company pursuant to National Instrument 43-101. The executive summary of the 2018 PEA, and subsequently a technical report will be posted on the Company’s website and filed on SEDAR within 45 days.

The PEA was conducted under the overall review and supervision of CSA Global Geosciences Canada Ltd of Toronto Ontario with the following Qualified Persons contributing to their respective sections. The listed Qualified Persons have reviewed the data contained in this news release and verified that it is accurately disclosed.

| Felix Lee | P.Geo., Principal Consultant, CSA Global Geosciences Canada |

| Ian Trinder | P.Geo. Principal Consultant, CSA Global Geosciences Canada |

| Scott Zelligan | P.Geo., Independent Resource Geologist |

| Bruce Brady | P.Eng., Senior Associate Mining Engineer, CSA Global Geosciences Canada |

| Chris Campbell-Hicks | P.Eng., Senior Associate Metallurgist, CSA Global Geosciences Canada |

| Gordon Watts | P.Eng., Senior Associate Mining Engineer, CSA Global Geosciences Canada |

Mr. Darren Koningen, P.Eng, a ‘Qualified Person’ as defined under Canadian National Instrument 43‑101, is responsible for the other technical information (information not directly related to the PEA) in this news release.

About Minera Alamos:

Minera Alamos is an advanced stage exploration and development company. Its growing portfolio of high-grade Mexican projects includes the La Fortuna open pit gold project in Durango and the Guadalupe de los Reyes gold/silver project in Sinaloa as well as the now combined Santana/Los Verdes gold-copper project in Sonora. The Company is well financed to conduct all of its planned exploration and development activities and continues to pursue additional project acquisitions in Latin America.

Imperial Metals Corporation (TSX:III) reports financial results f... READ MORE

Orezone Gold Corporation (TSX: ORE) (OTCQX: ORZCF) reported its o... READ MORE

Elevation Gold Mining Corporation (TSX-V: ELVT) (OTCQB: EVGDF) i... READ MORE

New Gold Inc. (TSXNGD) (NYSE American: NGD) is pleased to announc... READ MORE

PLANS FOLLOW UP DRILLING ON EXTENSIVE HIGH-GRADE COPPER-GOLD TARG... READ MORE