The Fed raised interest rates by 25 basis points. In response…not that much happened.

Sure, Treasury yields rose a bit. And stocks gained some. And gold rose. But the moves were small relative to gyrations we’ve seen in recent weeks.

So what now?

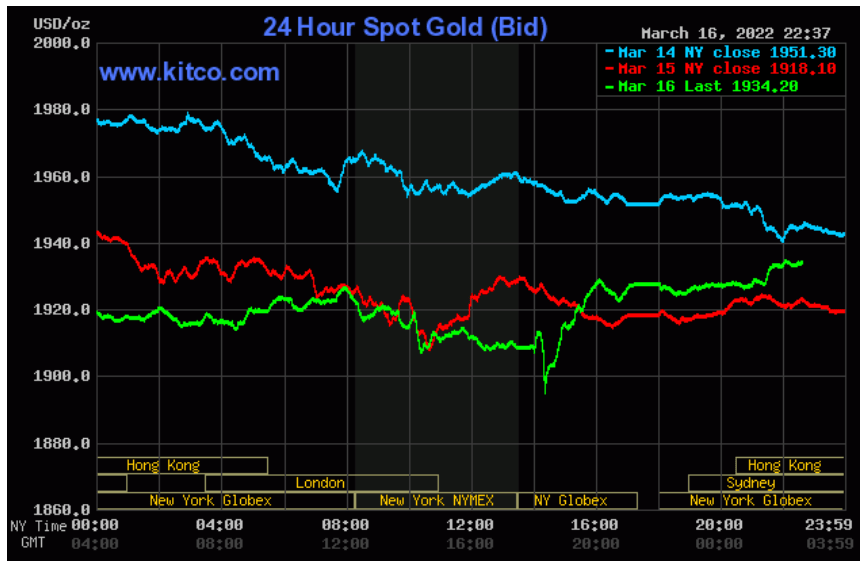

Gold had been trending down since peaking at $2,052 per oz. last week. I don’t even know what to say about that other than the usual: big moves have to consolidate, geopolitical moves aren’t usually as sticky as economic ones, and gold likes to slide into rate hikes.

Now it’s possible that the rate hike provided a bottom for this slide. That would make fundamental sense and would fit historic patterns. So far so good, but it’s only been 8 hours since the hike.

Rates from here: The new Dot Plot shows a range of opinions from the committee members but they cluster clearly around rates at just under 2% by the end of the year. To get there, the committee would enact another 0.25% raise at each of the six remaining meetings this year.

This is a balancing act. Hike too quickly and they’ll bring inflation under control alright – by destroying demand via a recession. Hike too slowly and inflation will continue its significant 10 drain on everyone’s purchasing power. The Russia-Ukraine war only made things harder by pulling several key inflation drivers – including energy – largely outside of domestic influence.

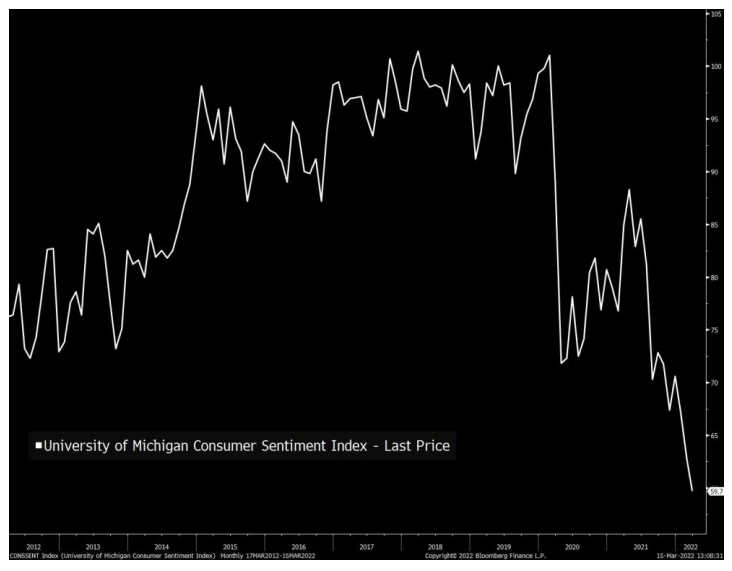

Powell is acutely aware of this balancing act. But he said in today’s press conference that he thinks “the probability of a recession within the next year is not particularly elevated.” I don’t know whether he’s right – and I’m not alone. One of the most confusing things today is the disconnect between consumer sentiment and what the data say.

Measures of consumer sentiment are in the basement.

But that stands in opposition to 5.7% GDP growth, a robust job market, soaring household net worth, and strong inflation (that until a few weeks ago was largely demand-pull inflation).

So why are consumers so negative? It’s hard to know, but it matters because the US is such a consumer economy. My guess is that, having gone through the Great Financial Crisis, the Taper Tantrum market correction, and the COVID crash, people are hesitant to expect a lot. Maybe warning signs like hot inflation are having more impact than before. Maybe returning to ‘normal’ after the pandemic is harder, financially and emotionally, than the numbers suggest.

Whatever it is, consumers are uncertain about economic growth ahead – and now the Fed agrees, having just downgraded its expectation for GDP growth in 2022 from 4% to 2.8%.

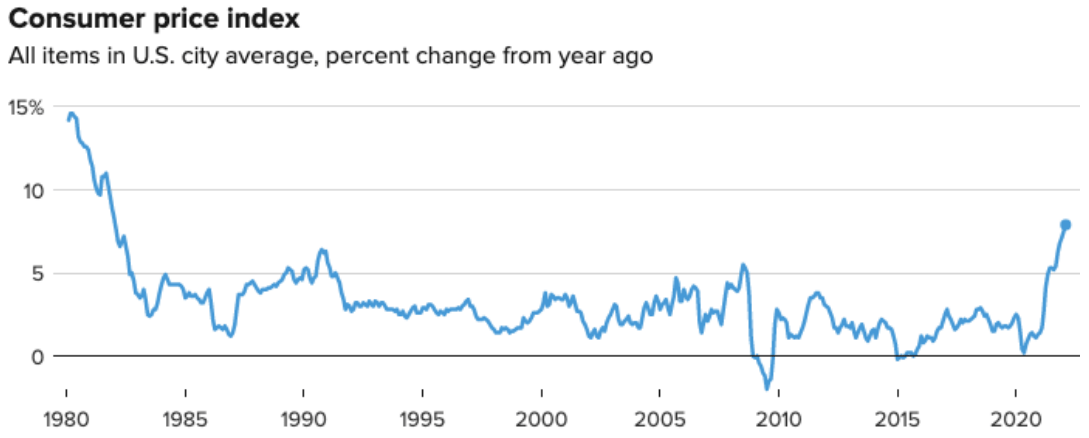

The Fed is much more optimistic on inflation. The median inflation expectation among Fed committee members is now 4.3% over 2022. Given inflation came in a whisker below 8% in February, it would have to moderate rapidly to average 4.3% for the year. Very optimistic.

I don’t know how they can be so optimistic. Inflation had climbed way above its range from the last 40 years before Russia invaded Ukraine. The war has only added inflationary pressure.

Will rates rising to 1.9% over the next year do anything to inflation? Debateable. As a starting point, I think most everyone agrees that the war has added a clear layer of demand-pull (demand is higher than supply for energy, wheat, fertilizer, and other commodities because countries are avoiding Russian output) to the cost-push that has driven inflation until now.

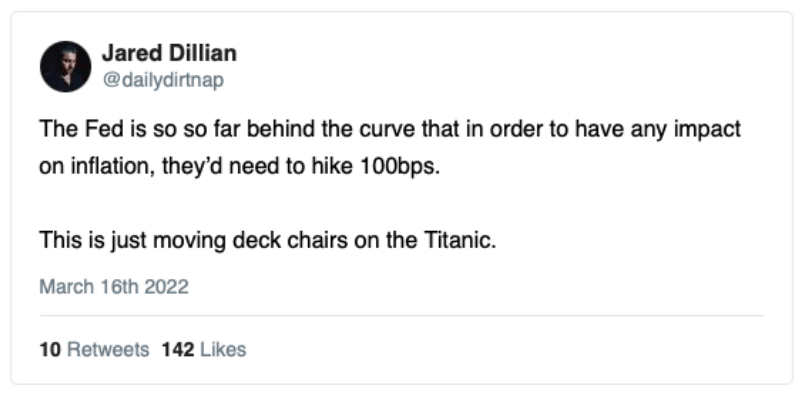

In terms of the debate, there are lots out there who think that 0.25% rate hikes aren’t anywhere near enough to have an impact.

Then there are all the folks who think inflation will take care of itself: food, energy, and housing will soak up everyone’s cash, completely drying up the demand-pull side of things. Maybe that explains the poor consumer sentiment – every trip to the grocery store, let alone the gas station, reminds the consumer that he/she better rein in discretionary spending to make ends meet.

I don’t know which is right. I am worried that inflation will cause a recession, either on its own or by prompting the Fed to hike rates too fast. The recession risk threatens base metals, because they are a proxy for growth. It supports gold, outside of whatever losses the yellow metals endures in the initial rout (baby with the bathwater).

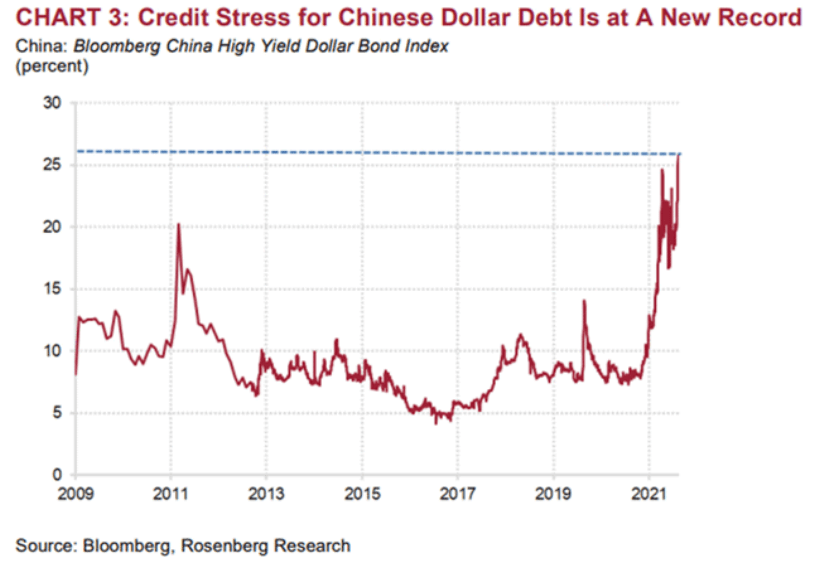

Worst case scenario, this all leads not to a recession but to a global depression with widespread food insecurity and rampant energy costs. Governments must subsidize food prices and end up unable to service foreign debts, especially if the US dollar keeps strengthening (global inflation like we have now, means the dollar could still strengthen as the cleanest shirt in the dirty laundry pile). This chart from David Rosenberg shows that kind of stress starting to show: huge piles of dollar-denominated debt re under great pressure in China.

Best case scenario, Ukraine and Russia agree to a ceasefire or peace deal of some sort soon. Russia withdraws its forces. Some sanctions get lifted, easing some of the demand-pull driving inflation by adding supplies back to the system. With the fear of rampant inflation eased, growth gets back on track.

But this best-case scenario is not likely. Just this morning, Putin called Russians who oppose the war “scum and traitors”, which doesn’t sound like a leader about to sign a peace deal. In addition, Russia’s pariah state will last much longer than the war so even a deal will only moderate, not erase, the impacts.

Neither scenario is great. Both deserve a few additional thoughts.

First, governments and central banks pulled out all the stops to support their citizens financially during COVID. I can’t imagine they would suddenly become tight-fisted with cash should a Russian war drive food and energy costs through the roof. If printing presses are needed, governments and central banks are now practiced at turning them on. China did a version of this already, today announcing stronger measures to support economic growth. Base metals immediately traded higher. And the potential need for the support given Russia’s war 13 is exactly why the FOMC only raised by 0.25% today – three weeks ago inflation expectations were lower and yet the market expected a 0.5% increase.

Second, the US is starting this challenge from a strong position. Unemployment is only 3.8%. GDP growth is still good. Manufacturing and inventory numbers are strong. Household savings are very high. There’s some cushion.

Third, the worst-case scenario is really bad but, as long as things don’t go quite that wrong, economic strength and household wealth could keep the economy and market chugging along as the inflation peak runs its course. In that context, gold would likely do very well and base metals would falter but recover and then respond to the realities of supply gaps to enact the green revolution.

Bonterra Resources Inc. (TSX-V: BTR) (OTCQX: BONXF) (FSE: 9BR2) i... READ MORE

Increased facility footprint reflects advanced construction progr... READ MORE

Aris Mining Corporation (TSX: ARIS) (NYSE-A: ARMN) announces the... READ MORE

Zodiac Gold Inc. (TSXV: ZAU) a West-African gold exploration co... READ MORE

Appia Rare Earths & Uranium Corp. (CSE: API) (OTCQB: APAAF) (... READ MORE