QUESTION:

I am trying to understand risk and time frames with miners. I just read this and wonder if it seems correct in your experience:

Stage 1: Exploration

This step is challenging and extremely complex. Considerable time, money and expertise in everything from geography to geology, chemistry and engineering are needed.

Interestingly, less than 0.1% of explored areas sites and just 10% of deposits will bring about a productive mine to justify development.

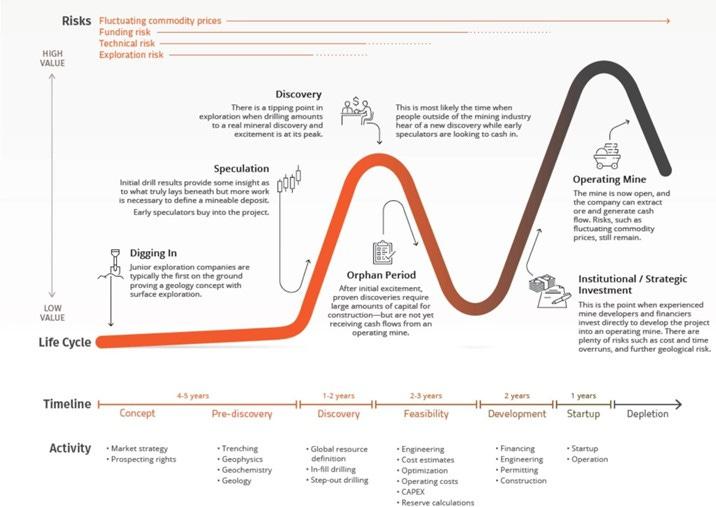

I am also looking at the Lassonde Curve. Maybe 2 years or so is a good time frame to be in and out? Like the Discovery and Development stages? Of course it’s hard to hit exactly the right spots on the curve but I want to aim properly. I want to adjust my portfolio away from long term timeframes for in/out.

— Reader LO

This is a great question because it hits at the core question every investor should be able to answer for his/her metals portfolio – what are you trying to achieve?

Are you buying explorers for the 1 in 1000 odds of success? (Yes, those odds are better with good geologic and market knowledge, but they’re still low.) Are you buying developers for the re-rate that comes with a successful mine build? Those are the two opportunities that the Lassonde Curve illustrates.

In a good market there are other opportunities. In a supportive metals market, companies gain in value as they turn discoveries into good, large resources (resource expansion). Companies can also transform in value if they buy an asset – a good asset deal really manifests the intangible value of managements’ connections, vision, and deal-making expertise – or if they get bought. Can’t put those on a chart because they don’t always happen, but they certainly matter when they do happen.

So let me get back to the beginning of your question.

Yes, those odds look about right to me. Exploration is a low success game in terms of making discoveries that become mines. As for estimating my success rate…well, that requires a deeper look at the question.

Success with investing varies person to person. I think it’s safe to assume that, when it comes to investing in tiny junior explorers, success is at least doubling your money within a reasonable timeframe (within two years?). I pegged it at doubling because we need our winners to win notably to compensate for our losers.

If that definition is reasonable, it’s important to realize that we don’t need a discovery to actually become a mine for the bet to win. You just need to own the stock during part of one of those Lassonde upswings, or during successful resource expansion in a supportive market, or when the company deals for a great asset or spins an asset into a new company that works or gets acquired.

That investing success is not limited to discoveries that become mines is the beauty of knowing what game you are playing. It leaves my ‘success’ track record with explorers at something like one in ten, even though almost none of my ‘success’ projects are now mines.

On the flip side, not understanding the game leaves you exposed to the bad periods in a stock’s trajectory. And the Lassonde Curve is too kind on that front, I should note. First, it shows the pre-discovery phase as a boring but still slightly ascending wait. As we all know, it’s often much worse than that.

Second, it suggests that the Orphan Period is only 2-3 years. I wish. I’d say investors get bored of a new discovery sometime around the prefeasibility study and don’t get interested again until it’s half built. If a project maintains momentum from PFS to operation without pause, that’s easily five years and often ten, depending on permitting. And most of the time a bear market will get in the way and put the project on pause for several or maybe many additional years.

As for the time frame from investing to discovery success – how long I’m willing to wait – that’s another very good question. There’s no simple answer but there are a few solid guidelines.

The biggest guide comes from the company’s exploration plan. If there is one compelling target to test: what happened? If there are multiple targets: what did they learn from drilling one of them? If there is more than one project in the mix: do you as an investor like all of them and how do your preferences align with the company’s plans?

I buy exploration companies because I think they have a compelling project that deserves a test. I re-assess that thesis after each round of drilling. If the project becomes less compelling, it’s time to exit. If it remains as compelling or gets better, it’s likely worth holding on.

It’s hard to discuss that process in terms of time because several factors impact how long it takes to give a project a good test. Is the project only accessible in the summer? Are markets supportive such that the company can raise enough money make good strides on the test with each exploration program? Did anything else crop up to get in the way, like weather (floods, fires, etc), access issues, permitting, or politics?

Even though those factors vary widely, my arm-waving response is that there should be enough progress on the test after one year for an investor to decide whether he/she thinks things are progressing well or not. That is not to say that a year is necessarily enough time to make a discovery! But it should be enough time to get a round or two of exploration done, which should generate enough information to decide whether you’re still interested.

It’s up to the company, I should note, to explain why you should remain interested. They’re the geologists, so it’s up to them to explain why the data is encouraging. If they fail to do that, it’s a red flag – either the data isn’t all that encouraging or they aren’t good communicators, which is a big problem when your job is to tell and sell a story.

Time is money, so I wouldn’t wait for longer than two years for a discovery on the original thesis. I will note that I might hold an explorer longer than that if the company shifts focus to another project and I like that opportunity, but two years on one project without a discovery is as much as I’m willing to wait.

Not waiting longer is not about patience. It’s about two things: the time-value of an investment that isn’t working and that, the longer it takes an explorer to make a discovery, the harder it becomes for that stock to succeed. On the first: your money could be generating returns elsewhere were it not locked up in this struggling stock. On the second: every month costs in salaries, accounting, marketing, office space, and property payments while every program costs in sampling, drilling, and manpower. Failure is expensive, erodes the saleability of the story, and dilutes the share structure.

So assess after a year (if you haven’t assessed when the company issued exploration results) and exit after two years if there hasn’t been a discovery.

What if there has been a discovery? I’ve talked before about discovery price spikes: how investors excitement over a new discovery often sends the share price well beyond where it deserves to be. That’s a great opportunity to sell some, reducing or taking back all of your capital on the table, or just to exit if the price spikes dramatically.

If you hold beyond the discovery price spike, it has to be because you think the market hasn’t understood the potential of the discovery. Maybe there’s a geologic reason. Maybe there are lookalike targets that haven’t been drilled yet. Maybe a weak market means the discovery went relatively unnoticed. Maybe the story shifted in an important way that’s not being noticed.

That last example happened with Great Bear. I pounded the table on buying more Great Bear as that team started drilling the LP Fault because I realized the market was still pricing the stock for its narrow high-grade veins and hadn’t realized the value in the huge, gold-endowed LP Fault.

Long story short: in a reasonable to good metals market, discovery price spikes are often the best time to take your money and exit unless you have a clear reason to believe there’s more potential at the project than the market realizes.

As for buying developer stocks for the re-rating they should enjoy upon successfully commissioning a new mine, the entry and exit points there are more clear.

If you find that you hold stocks for longer than you’d like, it’s possible you haven’t applied sufficient constraints to your explorers, have entered developers too early, or have other investment concepts that lack timeline requirements.

For explorers, it’s important to establish a detailed investment thesis for each stock and then to assess the company’s progress against that thesis at least annually. If you don’t, then you’ll end up holding all kinds of explorers for ages while they pursue this target and that idea.

Explore co’s will always have a new idea; the question is whether it’s an idea you would actively buy.

For developers, it’s easier than you think to make the mistake of entering during the orphan period. Projects going through feasibility studies and permitting can sound appealing because they are so well understood; the guessing about what the rocks hold is over, replaced by knowledge of tonnage and grade and how it will be mined. And management teams in this phase will always provide reasons to enter, whether because they project might get bought or because of exploration targets they’re advancing or because the commodity in question is rising and their asset offers leverage. And yes – a takeout might happen (but usually doesn’t), exploration might work (but has to be hugely successful to impact the value of a feasibility- stage project), and the metal price might rise (but there are other ways to have exposure, and leverage, to such an opportunity).

As for other investment concepts that might drive you to buy, the most common is the idea of a takeout. To be sure, we would all buy stocks of any stage if we could reliably predict a pending takeover. But it’s impossible. Stage doesn’t help, as some projects get bought pre resource while others aren’t bought until they’re built, and everything in between. The bigger the resource, the more economic the mine plan, the less fraught the jurisdiction – these things all make a project more appealing to majors but none provide a guarantee.

And so buying a stock on the bet it will get taken out fails far more often than it succeeds. But since no one likes being wrong, it’s very easy to keep waiting…which can certainly keep stocks in your portfolio longer than you’d like.

It’s all about the investment thesis. Have a clear one for each stock, check in with it regularly, and don’t let dreams of rising tides or takeouts keep you in a stock if the thesis breaks down.

I’m wondering which of the following scenarios is likely best for shareholders:

— Reader JP

While it’s hard to simplify all the potential scenarios in play, the best outcome is usually to have the company acquired for cash.

Having the project acquired gives the company a bunch of cash. That can work well for the stock, as cash fuels the rest of the company’s plans, but cash also doesn’t last and isn’t guaranteed to generate new value so its impact often erodes.

It’s much cleaner if the whole company gets acquired for the target asset. If there are several other assets, the deal often includes spinning those other assets out into a new company that shareholders get to own, which can be a nice bonus.

When there is a company takeover, cash is better than shares. For one, it usually takes months for a deal to close and the buyer’s shares trade that whole time. That means the market gets to decide the value of share-payment deals – if opinion is negative, the buyer’s share price will slide and shareholders of the company being acquired will get less than originally promised or intended. Of course, it can go the other way – the buyer’s share price can trade up before the deal closes – but that’s less common.

Mergers rarely create significant new value quickly. I know that sounds cynical, but it’s true.

Certainly in time they can work – synergies in operating mines or development projects and reduced G&A can create more value over time than the companies would have created on their own – but it usually takes time.

As for building a mine – this can certainly work! One of my top picks right now includes a mine-building team that took over a project that was being poorly planned, created a totally new approach, and financed, permitted, and built a mine that I think will shine. But it worked because building a mine was the investment thesis all along. Sure, there was always the chance they would get taken out along the way but I was confident in owning the stock if that never happened because I believed in the project, plan, and team.

All that said, building mines is a risky business. That’s why exiting just as a new mine enters production before the realities of mining have the chance to derail the stock, can work really well. It’s also really important that you only think about holding a stock through mine building if that’s the thesis from the start. You certainly don’t want to hold onto a discovery because you think it might make a good mine because it takes at least a decade, if not several, to move from discovery to production. That kind of timeframe will always include a bear market and the long, painful for shareholders orphan period.

Takeouts are great because they almost always come with a premium, something like 30 to 50% above where the stock is trading. And for a stock to get taken out for cash is the simplest outcome. Building a mine can also certainly work, though it takes time, expertise, and a bit of luck.

Courtesy of the Resource Maven

Namibia Critical Metals Inc. (TSX-V: NMI) (OTCQB: NMREF) is pleased to announce that Japan Organizat... READ MORE

Eldorado Gold Corporation (TSX: ELD) (NYSE: EGO) today reports the Company’s financial and operati... READ MORE

DPM Metals Inc. (TSX: DPM) (ASX: DPM) announced its operating and financial results for the second q... READ MORE

IMC Rare Earths Ltd, a company focused on the mineral exploration and development of magnet rare ear... READ MORE

Fairchild Gold Corp. (TSX-V: FAIR), is pleased to announce the closing, on July 29, 2026, of its pre... READ MORE