These are such headline-driven days. Stock markets dropped yesterday when news broke of the Democrat’s move to start impeachment proceedings against President Trump. Then they rebounded this morning when the transcript of Trump’s Ukraine call was released and turned out less damning than some had expected. Gold did the opposite, gaining yesterday and then falling today.

Someone asked me whether today’s (Friday) trading action in gold was concerning. Short answer: no.

First of all, these are headline-driven days. Stocks, bonds, gold, oil – they all jump and dive on the news cycle. However, the vast majority of those moves are fairly small in context. I saw one headline: “S&P 500 drops the most in a month on Trump impeachment concerns.” The most in a month? Is that really worth noting?

Gold’s slide today is similar. It too likely dropped the most in a month, but that dramatization misses two key points:

Headlines do matter, but the details that spark reactions one day fade quickly. What matters are the themes.

And those themes remain:

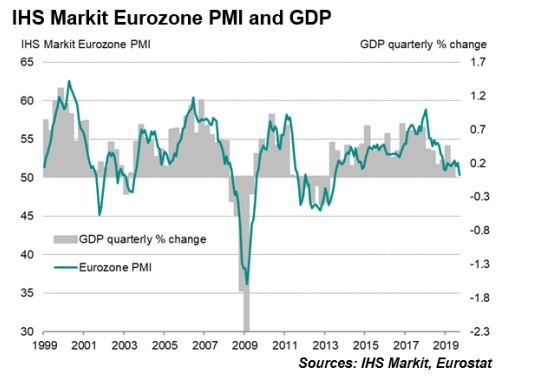

· Uncertainty. The EU is truly on the edge of recession (the Flash Eurozone Composite PMI reading, which combines manufacturing and services, was 50.4 for September, barely above the 50 mark that signals contraction; manufacturing is already in contraction). The trade war drags on. Central banks around the world are cutting rates; several are already injecting stimulus. China is struggling to keep its currency stable (to keep trading partners happy) while managing an ongoing debt crisis.

A messed up bond market. With a quarter of investment grade bonds bearing negative yields, the safe haven trade truly is different this time. Large pools of money that have long relied on bonds for reliable returns are being forced to look elsewhere. Stocks worked for several years but now, based on the three points above, risks are rising.

More and more, I think an important theme (that brings all of these together) is the self-fulfilling nature of recessionary fears. Crescat Capital summed this idea up nicely in a recent letter called Necessary, Normal, and Inevitable, in which they predict a recession is imminent partly because investors increasingly think one is around the corner, as well as because evidence is piling up.

Gold is an answer for all of these themes. That’s why the chart looks so strong. And that’s why I don’t stress when the news cycle sends the yellow metal down on a particular day.

I’ve gone through the gold equities argument many times. In short: gold bull markets start with the metal itself. As the price of gold gains, gold producers start to move; they offer leverage to the gains in price (they make more money, assuming fairly fixed costs) and they are large, liquid stocks.

It’s only after that is well and truly established (a point we’re not even quite at yet) that money starts to really rotate down into more speculative stocks.

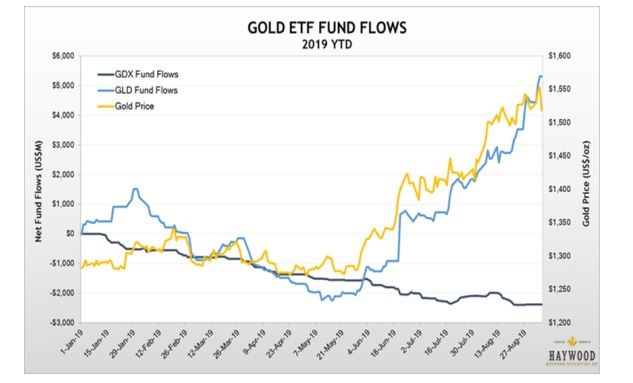

In fact, even though gold majors have seen very nice gains in this market already (50 to 100%), fund flows into such stocks have remained pretty limited. This chart from Haywood captures things nicely.

The golden line is the price of gold, the blue line is funds flowing into gold-backed ETFs, and the black line is funds flowing into the main ETF of gold mining stocks, the GDX. The divergence is just slightly apparent.

It means there is lots of room for equities to gain once generalist investors decide this market is real and they want to participate.

New Gold Inc. (TSX: NGD) (NYSE American: NGD) is pleased to annou... READ MORE

Silver Viper Minerals Corp. (TSX-V: VIPR) (OTC: VIPRF) announces... READ MORE

MAX Power Mining Corp. (CSE: MAXX) (OTC: MAXXF) (FRANKFURT: 89N) ... READ MORE

70,000 meters completed, highlights include: 349.0 m of 0.77... READ MORE

Rupert Resources Ltd. (TSX:RUP) reports assay results from projec... READ MORE