PDAC says 23,819 people attended this year’s conference. It’s an impressive number after a modest show last year and a missed show in 2021. And you might think such strong attendance suggested good investor interest in the mining space.

But the newsletter writer session, which is arguably the best place in a sprawling conference to gauge retail investor interest, looked like this:

Both Toronto conferences felt very mixed. Day one of the Metals Investor Forum was quiet; day two was busy. At PDAC, the audience for the newsletter session was thin but the convention floor felt busier. As for outlooks, in conversations I heard optimism that gold will perform come what may, excitement over certain small market green metals like tellurium, doomsday calls for the stock market and economy and base metals in the near term, and enough opposing opinions for all of those that it was impossible to capture any clear ‘conference sentiment’. (Of course, those opinions were all voiced before the banking crisis.) There were a few themes worth noting, though, and top among those is consolidation.

I’ve said many times that there’s a shortage of advanced gold projects that miners could buy to restock reserves and support future production. Supporting future production is increasingly important, as most miners see output slip more each year. For instance, industry leader Barrick announced 2022 production that marked a 22-year low. A dearth of deals in the last decade means these trends are expected to continue.

I think the stage is set for M&A to ramp up across the mining space this year, for a few reasons.

Bigger Is Better. Last month Newmont bid for Newcrest in what would have been a mega $17- billion deal. Newmont did so because it wants to be big enough to matter.

What? Newmont is one of the two biggest gold miners in the world! How can I say Newmont isn’t big enough to matter??

I can say it because the gold space is tiny, so even its largest players are miniscule in the grand scheme of the stock market. And size matters in a market where indexing gets more important every year.

Size is a very common parameter for inclusion in an index. And being included in an index means a stock sees buying, often significant buying. But gold majors are too small to get in the game. So Newmont wants to buy/merge with Newcrest as part of an effort to get big enough to matter in the broad markets.

I’m sure Newmont isn’t the only miners thinking this way. The bigger they get, the more indexes they’re eligible for and the more passive buying they can thus get. It’s a growing force across the gold sector.

Not Waiting Anymore. If the almost 24,000 people at PDAC were not investors, it’s fair to wonder who they were. The answer gets to why PDAC really exists. They were geologists and executives from companies in the space, from the very largest miners to the smallest explorers, and they were there to talk to each other.

Deals are often born at PDAC. And between the shortage of good advanced assets and the need to grow to be noticed, I know a lot of potential deals were aired. I increasingly get the sense companies in the mining space can no longer wait for investors to get interested before doing deals; they want to transact and grow now. At last count there were eight M&A deals underway in the gold space alone.

(There are also many thousands of suppliers, consultants, government representatives, indigenous groups, and media at PDAC, I should note.)

More Players, More Pressure. Another theme that I heard discussed a lot was that downstream users were present and busy at PDAC and the surrounding events. Car makers, battery manufacturers, electronics companies – they all want to secure access to metals they know will be in short supply in the coming years.

Downstream users figuring out how to get a foot in the door of future project isn’t new in the mining space but it is increasing every year. That so many were present and busy at PDAC this year was a good reminder that miners will not be the only actors in this base metal M&A cycle. More actors will mean more pressure to act, once the bids start really flowing.

I think we’ll see M&A action rise through 2023 regardless of the macro environment, especially in gold but also across base metals. Each year a miner has fewer tonnes of resource left in the ground. The only way to stay alive is to buy and build. And smaller players – single asset operators and developers – also see this coming and also want to grow.

Once it starts, an M&A trend could gather steam because there just hasn’t been enough buying or building in the last decade, so new asset needs are high. But the inventory of new assets is low. If I’m right, deals could be the spark this space needs.

Of course, the gold space also need generalist interest. It’s not here yet but if gold stands out as a risk hedge in the coming months and then as a contrarian move when a recession hits, we could finally see the level of investor interest needed to create a real gold bull market.

To start, we need traditional gold investors to get back on board. This group – myself included! – lost a bit of faith in the first two months of 2023 because rising rates and economic strength weakened the arguments for gold to perform in the near term.

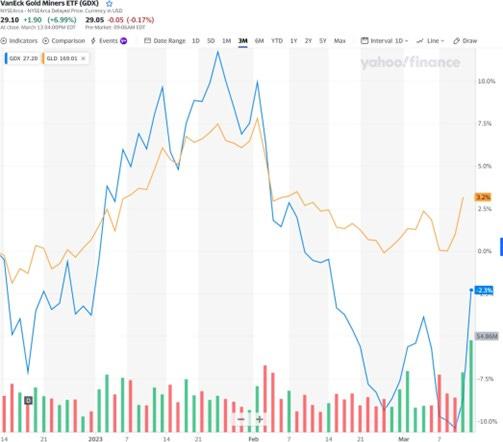

You can see that in the chart of gold (as per GLD, the yellow line) versus gold miners (as per GDX, the blue line) below. Miners underperformed gold in January and February. The events of the last few days look to have brought traditional interest back to gold equities. That’s step one complete!

Namibia Critical Metals Inc. (TSX-V: NMI) (OTCQB: NMREF) is pleased to announce that Japan Organizat... READ MORE

Eldorado Gold Corporation (TSX: ELD) (NYSE: EGO) today reports the Company’s financial and operati... READ MORE

DPM Metals Inc. (TSX: DPM) (ASX: DPM) announced its operating and financial results for the second q... READ MORE

IMC Rare Earths Ltd, a company focused on the mineral exploration and development of magnet rare ear... READ MORE

Fairchild Gold Corp. (TSX-V: FAIR), is pleased to announce the closing, on July 29, 2026, of its pre... READ MORE