I’m starting with that because the second sentence sets the scene: “With money coming out of bonds and looking for new inflation-proof homes, commodities are likely to attract investors…”

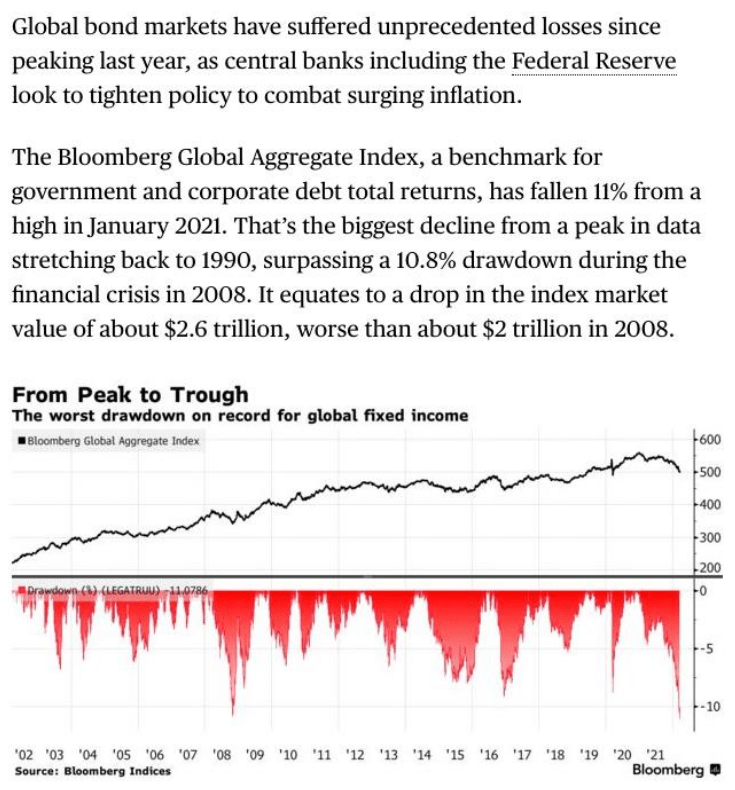

And money is coming out of bonds. The screen capture below is from a Bloomberg article.

Tuesday’s brutal selloff eased today but tomorrow is another day…and the same forces remain in play: rising inflationary pressures around the world are (1) pushing central banks to raise rates and (2) fueling concerns about whether the global economy can handle rampant inflation and higher financing costs.

I’ll get back to point (2) in a moment. On (1), no one knows. And until there’s some clarity, all anyone can do is try to position for what might be.

OK, so what is an investor to do when inflation rages? It depends on the reason for the rage. When inflation stems primarily from strong demand (Demand Pull inflation) the Go To investment answers are commodities, stocks, and gold.

Commodities work because growth can’t happen without them, so demand remains strong, and because they are generally priced in USD, so inflation essentially benefits the play.

Stocks work because strong economies can handle inflation surprisingly well. Companies pass increased costs on to consumers, who can keep buying in a true demand-pull inflationary setting because wages rise with inflation. That preserves earnings and earnings are the most reliable correlation with the direction of the S&P 500.

This is why stocks have gained 5 of the last 6 sessions, erasing half of the steep losses from January and February even as war rages in Ukraine and the Fed raises interest rates. It seems some are buying because stocks sometimes hedge inflation. Others are buying for lack of a better option (bonds? Cash?). And there are probably some buying stocks not despite rising rates but because rates are rising, as they think higher rates will work better for stocks than entrenched inflation.

And gold works because it’s a commodity and because it’s the hedge for when everything else stops working. Never forget that rate hikes are a blunt tool; they temper inflation by destroying demand. At some point consumers slow buying because wages can’t keep up, prices get nuts, and mortgage and rent payments come first. Lack of buying slows growth. It’s near impossible to do this gently, so it usually leads to a recession…and of course stocks don’t perform in a recession. Enter gold, the hedge for that inevitable endpoint.

That’s Demand-Pull inflation in a strong economy. Things are different for Cost-Push inflation, wherein prices rise not because lots of money is chasing limited supply but because other forces are raising costs.

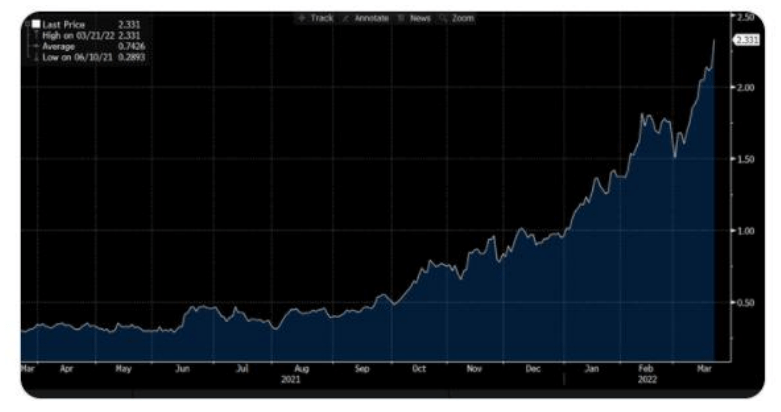

The war in Ukraine is a prime example – oil and natural gas in Europe prices did not surge because of a sudden rush of demand but because of a sudden, major constraint on supply. Those higher prices have forced manufacturers in Europe to reduce or suspend operations because they can’t afford energy, which is strangling supplies of aluminum, urea, copper, nickel, and zinc, for instance. The Tweet below shows an article in a Dutch newspaper; veggies are going to get more expensive in Europe because of Russia. Wheat prices jumped because a third of the world’s wheat comes from Russia and Ukraine. You get the idea.

So which kind of inflation do we have now? Both. Inflation was hot before Ukraine. The ‘transitory’ argument was, essentially, a cost-push argument: that inflation was coming from supply chain issues and would ease once those resolved. And that is likely how inflation started but a reviving post-COVID economy and easing of those supply issues turned it largely into Demand-Pull inflation. And now Russia has added a major layer of Cost-Push on top.

Econ textbooks don’t tell you what happens when you get a combination of Cost-Push and Demand-Pull inflation, because it’s not supposed to happen!

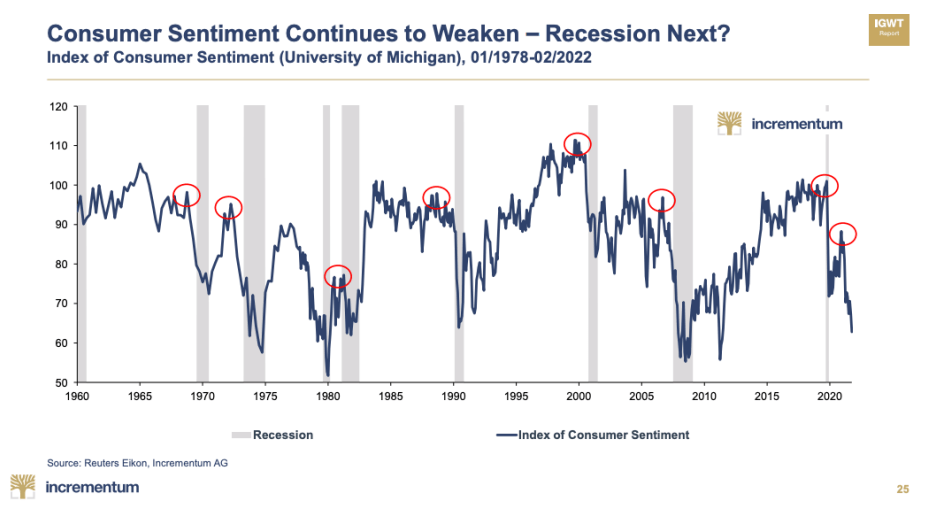

We do know that high inflation typically leads to a slowdown, which only makes sense: at some point wage hikes can’t keep up and consumers lose purchasing power and/or the central bank hikes to much or aggressively and debt costs drown growth. The thing to watch is manufacturing. ISM Manufacturing is a monthly indicator of economic activity at 300 US manufacturers and if it shows a weakening trend then we’ll know inflation is slowing growth. We’re already seeing consumer sentiment weaken, which is notable.

I don’t know if this weakening of consumer sentiment is significant as yet…but we all feel inflation every day, which at some point gives consumers pause on spending. And North America is a such consumer-driven market.

The jury is very much still out on the recession question. Stocks wouldn’t be surging if most people saw a recession coming. Certainly Powell doesn’t seem to see one coming, and it was his comments on that front that added fuel to the bond market rout.

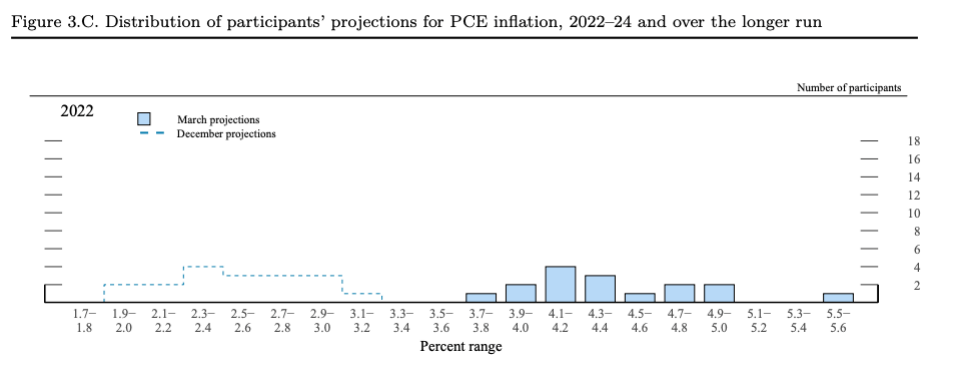

Before I get to those: the Fed’s official stance following last week’s meeting was much more hawkish than it had been three months earlier. In December, no one on the FOMC expected rates above 2.25% at the end of 2023. Now 16 of 17 members see rates that high. For central bankers, that’s a huge shift. They also significantly boosted their inflation outlooks: in the chart below the dashed line show their December forecasts while the solid line shows updated forecasts – but I have to admit even the updated outlooks made me think of the Tweet I’ve pasted in below.

Significant shifts notwithstanding, everything that came from the Fed was expected and so didn’t have that much impact. What did have impact was what Powell said in a speech on Monday:

“If we conclude that it is appropriate to move more aggressively by raising the federal funds rate by more than 25 basis points at a meeting or meetings, we will do so.”

The market immediately took that to mean the Fed could well raise by 50 points in May, given that inflation is very high and rising. As much as anything, the comment underlined that Powell is ok if stock prices fall, credit spreads widen, and bond yield rise if that’s what it takes to rein in inflation.

That seems obvious, as those outcomes are exactly what happens when higher rates put the brakes on growth. But investors have not had to live in reality for a long time. I regularly say the Fed hasn’t tightened in 12 years – they did raise rates between 2016 and 2019 and taper bond holdings, but all through those three years everyone knew they would step back the moment the stock market showed any stress. And that’s exactly what happened: the market cracked in late 2018 and within months rates were dropping hard.

That cushion, which became known as the Fed Put, is no longer in play. Powell saying in response to a question during last week’s press conference that he’s ok with a lower stock market to get inflation back in line cements it.

The Fed won’t act to support the stock market, not until/unless inflation is clearly on its way down. Yet in response stocks are rising as investors seek a place to put money that isn’t bonds, which are tanking.

The recession question will determine how the bet on stocks comes out. Rather than make that broad gamble, I’m keeping my bets on things that are more reliable in an inflationary environment: commodities and gold.

For base metals, glance back at the Scotia comment I included at the start. The upwards trend for most base metals is intact, excluding insane Russia-related spikes.

As for gold, the yellow metal has been taking it all in stride. Sure, on a daily basis the price has felt jittery, moving up or down by $40 to 60 per oz. on multiple days. But let’s put those tallerthan-usual red and green lines in context.

Gold surged with the start of the Ukraine war. It has given up some of those gains but only after re-pricing significantly higher. And gold continues to hold that ground in the face of strongly rising bond yields – in other words, it’s sticking higher despite higher (still negative, but not as negative) real rates.

Whether inflation is Cost-Push or Demand-Pull, whether the economy and by proxy the stock market are strong enough to survive this intense inflation or will falter later this year, whether rates rise 25 or 50 basis points at the start of May, a few things are clear. One: the Fed is badly behind on inflation so real rates are negative. Two: there is a huge amount that cannot be known right now, from how severe inflation will get to how the economy will handle is, so safe havens are needed. And three: commodities, including gold, perform with inflation.

Canadian Copper Inc. (CSE: CCI) announces that it has closed its ... READ MORE

New Pacific Metals Corp. (TSX: NUAG) (NYSE-A: NEWP) is pleased to... READ MORE

Thunder Gold Corp. (TSX-V: TGOL) (FSE: Z25) (OTCQB: TGOLF) is ple... READ MORE

5.17 g/t Au Over 2.9 Meters and 7.37 g/t Au Over 2.0 Meters VI... READ MORE

Abcourt Mines Inc. is pleased to present a major, unaudited opera... READ MORE