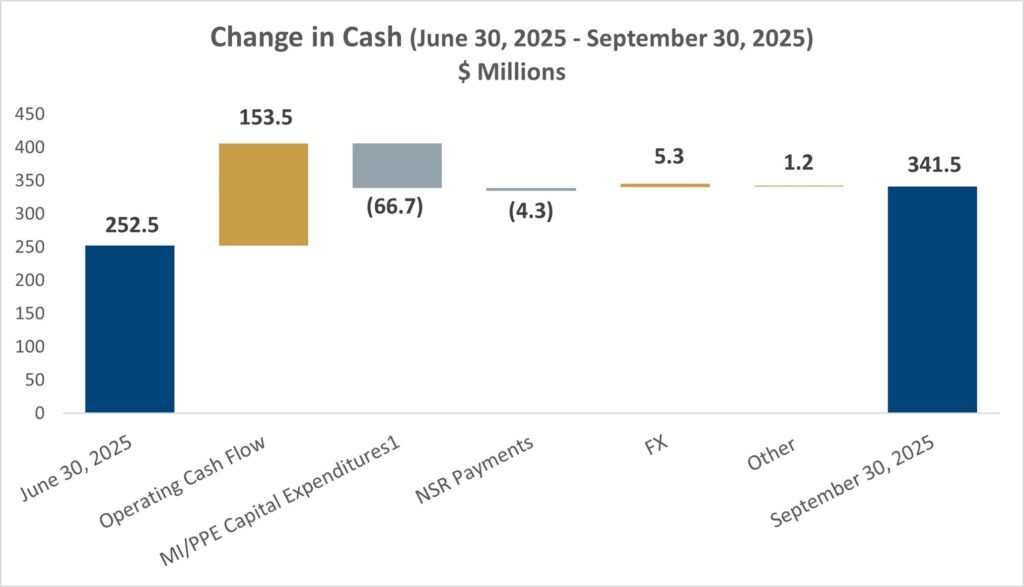

Cash of $341.5 million at September 30, 2025

Discovery Silver Corp. (TSX: DSV) (OTCQX: DSVSF) announced the Company’s financial and operating results for the third quarter and first nine months of 2025. Discovery began reporting the results of gold production and sales following the Company’s acquisition of the Porcupine Complex in and near Timmins, Ontario on April 15, 2025. The Company’s full financial statements and management discussion & analysis are available on SEDAR+ at www.sedarplus.ca and on the Company’s website at www.discoverysilver.com. All dollar amounts are in US dollars, unless otherwise noted.

Tony Makuch, Discovery’s CEO, commented: “During Q3 2025, we generated solid operating and financial results while at the same time continuing to integrate systems, align policies and procedures, strengthen management structures and advance investment programs at Porcupine. A key highlight of the third quarter was cash flow, with net cash from operating activities of $153.5 million and free cash flow1 totaling $86.8 million. Strong cash flow resulted from a 56% increase in gold sales, to 66,200 ounces from 42,550 ounces the previous quarter, and an increase in the average realized gold price1, to $3,489 per ounce sold. Driven by strong cash flow generation, we grew our cash position by 35%, to $341.5 million at September 30, 2025. With our current cash, as well as a new revolving credit facility for $250 million, plus a $100 million accordion feature, Discovery is very well capitalized as it moves forward with investment plans aimed at growing production, improving costs and maximizing value creation at Porcupine.

“A key component of the tremendous potential at Porcupine involves exploration. Last week, we issued our first exploration update, which included excellent drill results from resource conversion and expansion drilling at Hoyle Pond, Borden and Pamour, as well as very encouraging results at Owl Creek, which confirm the presence of high-grade mineralization three kilometers to the west of Hoyle Pond. We also announced the commencement of drilling programs at Dome Mine and the TVZ Zone. Dome and TVZ have the potential to become two new mining operations that could substantially grow production and value creation in Timmins. Drilling at Dome and TVZ is being conducted as part of studies to more thoroughly evaluate the projects, with these studies targeted for completion in 2026.”

SUMMARY OF Q3 AND YTD 2025 PERFORMANCE

| Three months ended | Nine months ended | |||||||||

| In $ thousands except per share amounts | September 30, 2025 |

September 30, 2024 |

June 30, 2025 |

September 30, 2025 |

September 30, 2024 |

|||||

| Revenue | 236,961 | — | 142,010 | 378,971 | — | |||||

| Production costs | 106,807 | — | 54,919 | 161,726 | — | |||||

| Earnings (loss) before income taxes | 71,114 | (3,860) | 24,510 | 89,172 | (9,503) | |||||

| Net earnings (loss) | 42,439 | (3,860) | 5,534 | 41,521 | (9,503) | |||||

| Basic earnings (loss) per share | 0.05 | (0.01) | 0.01 | 0.06 | (0.02) | |||||

| Diluted earnings (loss) per share | 0.05 | (0.01) | 0.01 | 0.06 | (0.02) | |||||

| Cash flow from (used in) operating activities | 153,488 | (1,192) | 67,081 | 214,492 | (12,206) | |||||

| Cash investment on mine development and PPE | (66,675) | (2,280) | (39,766) | (110,208) | (7,723) | |||||

| Three months ended | Nine months ended | |||||||||||

| September 30, 2025 |

September 30, 2024 |

June 30 2025 |

September 30, 2025 |

September 30, 2024 |

||||||||

| Tonnes milled | 808,688 | — | 508,791 | 1,317,480 | — | |||||||

| Average Grade (g/t Au) | 2.69 | — | 3.39 | 2.96 | — | |||||||

| Recovery (%) | 90.3 | — | 91.3 | 90.7 | — | |||||||

| Gold produced (oz) | 63,154 | — | 50,552 | 113,706 | — | |||||||

| Gold sold (oz) | 66,200 | — | 42,550 | 108,750 | — | |||||||

| Average realized price ($/oz sold)(1) | $ | 3,489 | $ | — | $ | 3,337 | $ | 3,430 | $ | — | ||

| Operating cash costs per ounce sold ($/oz sold)(1)(2) | $ | 1,339 | $ | — | $ | 1,341 | $ | 1,340 | $ | — | ||

| AISC per ounce sold ($/oz sold)(1)(2)(3) | $ | 1,734 | $ | — | $ | 2,074 | $ | 1,863 | $ | — | ||

| Adjusted net earnings(1) | $ | 61,090 | $ | (2,336 | ) | $ | 28,434 | $ | 86,479 | $ | (6,414 | ) |

| Adjusted net earnings per share(1) | $ | 0.08 | $ | (0.01 | ) | $ | 0.04 | $ | 0.13 | $ | (0.02 | ) |

| Free cash flow(1) | $ | 86,813 | $ | (3,472 | ) | $ | 27,315 | $ | 104,284 | $ | (19,929 | ) |

(1) Example of Non-GAAP measure. See the section in this press release entitled, “NON-GAAP MEASURES” for more information.

(2) For Q2 2025, ounces sold and the cash payments in the operating cash costs per ounce sold and AISC per ounce sold calculations that related to the Franco Royalty arrangement have been excluded. See the section in this press release entitled, “NON-GAAP MEASURES” for more information.

(3) YTD 2025 results exclude G&A expense, share-based compensation costs and sustaining capital expenditures and lease expense incurred prior to April 15, 2025, the completion date of the Porcupine Acquisition.

Q3 2025

(1) Represents cash capital expenditures incurred during Q3 2025

YTD 2025

Discovery did not generate revenue or earnings from mine operations in YTD 2024 or Q1 2025.

(1) Example of Non-GAAP measure. See the section of this press release entitled, “NON-GAAP MEASURES” for more information.

(2) Refers to earnings before interest, taxes and depreciation and amortization.

Income Statement Summary

| Three months ended | Nine months ended | ||||||||||||||

| September 30, 2025 |

September 30, 2024 |

June 30, 2025 |

September 30 2025 |

September 30, 2024 |

|||||||||||

| Revenue | $ | 236,961 | $ | – | $ | 142,010 | $ | 378,971 | $ | – | |||||

| Production costs | 106,807 | – | 54,919 | 161,726 | – | ||||||||||

| Depreciation and amortization | 35,826 | – | 16,384 | 52,210 | – | ||||||||||

| Royalties | 3,619 | – | 1,916 | 5,535 | – | ||||||||||

| Earnings from mining operations | 90,709 | – | 68,791 | 159,500 | – | ||||||||||

| Expenses | |||||||||||||||

| General and administration | 6,661 | 2,017 | 22,877 | 35,012 | 5,658 | ||||||||||

| Exploration | 5,972 | 158 | 830 | 6,827 | 375 | ||||||||||

| Impairment | 2,140 | — | — | 2,140 | — | ||||||||||

| Share-based compensation | 1,398 | 676 | 1,953 | 4,518 | 2,022 | ||||||||||

| Earnings from operations | 74,538 | (2,851 | ) | 43,131 | 111,003 | (8,055 | ) | ||||||||

| Other | |||||||||||||||

| Other income (loss) | 9,301 | (1,327 | ) | (6,879 | ) | 2,611 | (2,778 | ) | |||||||

| Finance Items | |||||||||||||||

| Finance expense, net | (12,725 | ) | 318 | (11,742 | ) | (24,442 | ) | 1,330 | |||||||

| Earnings before taxes | 71,114 | (3,860 | ) | 24,510 | 89,172 | (9,503 | ) | ||||||||

| Income taxes expense | 28,675 | – | 18,976 | 47,651 | – | ||||||||||

| Net (loss) earnings | $ | 42,439 | $ | (3,860 | ) | $ | 5,534 | $ | 41,521 | $ | (9,503 | ) | |||

| Basic earnings per share | $ | 0.05 | $ | (0.01 | ) | $ | 0.01 | $ | 0.06 | $ | (0.02 | ) | |||

| Diluted earnings per share | $ | 0.05 | $ | (0.01 | ) | $ | 0.01 | $ | 0.06 | $ | (0.02 | ) | |||

| Weighted average number of common shares outstanding (in 000’s) | |||||||||||||||

| Basic | 802,837 | 397,696 | 735,616 | 647,997 | 399,538 | ||||||||||

| Diluted | 825,798 | 397,696 | 762,923 | 670,958 | 399,538 | ||||||||||

PORCUPINE OPERATIONS REVIEW

Discovery’s Porcupine Operations cover approximately 1,400 km2 in and near Timmins, Ontario. Porcupine consists of the Hoyle Pond, Pamour and Hollinger mine properties, the Dome mine property and milling facility, and numerous near-mine and regional exploration targets. The Complex also includes the Borden mine property and large land position near Chapleau, Ontario. Current operations include the Hoyle Pond and Borden underground mines, with the Pamour open-pit project currently ramping up towards commercial levels of production. All mineralization is processed at the Dome, including mineralization from Borden, which is trucked 190 km to the mill. The Dome Mill is a 12,000 tonne-per-day processing facility that in recent years has operated at rates well below optimal levels. Through investment programs launched following the closing of the Porcupine Acquisition, the Company is targeting a return to full capacity operations by 2028 or sooner.

| Three months ended | Nine months ended | ||||||||

| Porcupine Complex | September 30, 2025 |

June 30, 2025 |

September 30, 2025 |

||||||

| Ore processed (t) | 808,688 | 508,791 | 1,317,480 | ||||||

| Average Grade (g/t Au) | 2.69 | 3.39 | 2.96 | ||||||

| Recovery (%) | 90.3% | 91.3% | 90.7% | ||||||

| Gold produced (oz)1 | 63,154 | 50,552 | 113,706 | ||||||

| Gold poured (oz)1 | 65,978 | 46,608 | 112,586 | ||||||

| Gold sold (oz)1 | 66,200 | 42,550 | 108,750 | ||||||

| Milling operating costs ($ Millions) | $ | 17,107 | $ | 12,861 | $ | 29,968 | |||

| Operating costs per tonne processed ($/tonne) | $ | 21.2 | $ | 25.4 | $ | 22.7 | |||

| Production costs | 106,807 | 54,919 | 161,726 | ||||||

| Operating cash costs per ounce sold2,3 | 1,339 | 1,341 | 1,340 | ||||||

| AISC per ounce sold2,3 | 1,699 | 1,849 | 1,756 | ||||||

| Total capital expenditures2,3(in thousands) | 65,976 | 41,632 | 107,608 | ||||||

(1) Includes gold production, poured and sold from Hoyle Pond, Borden and Pamour.

(2) Example of Non-GAAP measure. See the section in this press release entitled, “NON-GAAP MEASURES” for more information.

(3) Operating cash costs per ounce sold, AISC per ounce sold and total capital expenditures are site level and exclude remaining corporate G&A, share-based compensation costs and corporate-level sustaining capital expenditures.

During Q3 2025, a total of 808,688 tonnes were processed at Porcupine Complex at an average grade of 2.69 g/t, with recovery rates averaging 90.3%, which compared to 508,791 tonnes at an average grade of 3.39 g/t and recovery rates averaging 91.3% for the 76 days from April 16, 2025 to June 30, 2025 in Q2 2025. A total of 63,154 ounces of gold were produced over this period, with total gold poured of 65,978 ounces, compared to 50,552 and 46,608 ounces produced and poured respectively, in the previous quarter. Higher production in Q3 2025 mainly reflected the favourable impact of increased mining rates and higher average grades at both Borden and Pamour, partially offset by a reduction in mining rates and average grades at Hoyle Pond. During Q3 2025, production at Hoyle Pond was impacted by ventilation constraints during a period of high temperatures, which limited access to higher-grade area of the S Zone Deep.

Availability rates at the Dome Mill during Q3 2025 were impacted by a scheduled five-day maintenance shutdown in July for the purpose of replacing the discharge head and shell of B Rod Mill, rebuild of the tertiary crusher, and feeder repairs at the coarse ore stockpile. The Company used the occasion of the shutdown to advance multiple other projects, primarily in the grinding water system, repair to the mill reclaim water pond and carbon handling circuits. Based on operating days during Q3 2025, mill throughput averaged approximately 9,295 tonnes per day. Mill operating costs during Q3 2025 totaled $17.1 million for an average of $21.15 per tonne processed, which compared to $12.9 million and an average of $25.4 per tonne, respectively, the previous quarter, with the improvement in operating costs per tonne resulting from the 59% increase in tonnes processed. Mill costs are allocated to the mine operations based on a proportion of total tonnes processed.

For YTD 2025 a total of 1,317,480 tonnes were processed at Dome Mill at an average grade of 2.96 g/t, with recovery rates averaging 90.7%. A total of 113,706 ounces of gold were produced over this period, with total gold poured of 112,586 ounces. Total mill operating costs were $30.0 million for YTD 2025, for an average of $22.75 per tonne processed. The mill costs are allocated to the mine operations based on a proportion of total tonnes processed.

Production costs, including mining and processing costs, in Q3 2025 totaled $106.8 million versus $54.9 million in the previous quarter. Operating cash costs1 averaged $1,339 compared to $1,341 in the previous quarter. Site-level AISC1,2 averaged $1,699 per ounce sold compared to $1,849 in Q2 2025. Included in Q3 2025 AISC was $22.1 million of sustaining capital expenditures1, mainly related to capital development activities and capital expenditures related to the TMA6, which increased from $14.8 million in Q2 2025. The improvement in AISC was due to a 63% increase in ounces of gold sold, lower accretion and amortization of site closure provisions, partially offset by higher sustaining capital expenditures.

For YTD 2025, production costs totaled $161.7 million, with operating cash costs averaging $1,340 per ounce sold and AISC averaging $1,756 per ounce sold. Included in AISC were $36.8 million of sustaining capital expenditures related to capital development and expenditures related to the TMA6.

(1) Example of Non-GAAP measure. See the section in this press release entitled, “NON-GAAP MEASURES” for more information.

(2) Site-level AISC includes corporate G&A allocation and excludes remaining G&A, share-based compensation costs and corporate-level sustaining capital expenditures.

CORDERO OVERVIEW

The Cordero Project was acquired by Discovery in 2019. Since that time, the Company has invested over $100.0 million in Mexico, conducting significant exploration drilling and technical analysis, leading to the release of multiple studies, most recently the feasibility study dated February 16, 2024 and filed on SEDAR+ (www.sedarplus.ca) on March 28, 2024. The results of the FS confirmed Cordero to be one of the world’s largest undeveloped silver deposits, with the potential for large-scale production at low unit costs and that is capable of generating substantial free cash flow and attractive economic returns.

Key highlights of the FS include:

Third Quarter 2025 Highlights

During Q3 2025, Discovery continued work on key initiatives to further de-risk the project, including:

(1) AgEq produced is metal recovered in concentrate. AgEq is calculated as Ag + (Au x 72.7) + (Pb x 45.5) + (Zn x 54.6); these factors are based on metal prices of Ag – $22/oz, Au – $1,600/oz, PB – $1,00/lb and Zn – $1.20/lb (2) use in the February 2024 FS.

Example of Non-GAAP measure. See the section in this press release entitled, “NON-GAAP MEASURES” for more information.

OUTLOOK

With the closing of the Porcupine Acquisition on April 15, 2025, Discovery was transformed into a diversified North American-focused precious metals producer combining growing gold production in Northern Ontario, Canada, with one of the world’s largest silver development projects in Chihuahua State, Mexico.

Key priorities for the Porcupine Operations in 2025 continue to include:

The Company is currently executing a 140,000-metre drill program, which is expected to be completed early in 2026. The goals for the drilling program include resource conversion and expansion at Hoyle Pond, Borden and Pamour, in support of an updated technical report, to be issued in 2026, as well as the evaluation of district level targets, including Owl Creek, located approximately three kilometers west of Hoyle Pond. In addition, drilling is also being conducted at both Dome Mine and the TVZ Zone as part of studies to further advance and evaluate these high-potential targets.

With $341.5 million of cash at September 30, 2025, and the $250 million RCF, the Company is well capitalized to fund growth and optimization plans for Porcupine and current expenditure plans at Cordero.

In Mexico, the Company plans to further advance and de-risk the Cordero project, with key areas of focus being power, water availability and management, permitting, and the continuation of ESG and community outreach programs.

Following the completion of the land acquisition program in March 2025, the next major milestone for Cordero will be approval of the Company’s Environmental Impact Assessment or MIA by SEMARNAT, which was submitted in August 2023. The MIA passed SEMARNAT’s legal review soon after its submission and was advanced for technical review. As of the date of this press release, the Company had completed the technical review process and was awaiting approval of the MIA. The Company remains confident that Cordero will receive MIA approval.

ABOUT DISCOVERY

Discovery is a growing North American-focused precious metals company. The Company has exposure to silver through its first asset, the 100%-owned Cordero project, one of the world’s largest undeveloped silver deposits, which is located close to infrastructure in a prolific mining belt in Chihuahua State, Mexico. On April 15, 2025, Discovery completed the acquisition of the Porcupine Complex from Newmont Corporation, transforming the Company into a new Canadian gold producer with multiple operations in one of the world’s most renowned gold camps in and near Timmins, Ontario. Discovery owns a dominant land position within the camp, with a large base of Mineral Resources remaining and substantial growth and exploration upside.

Hudbay Minerals Inc. (TSX:HBM) (NYSE: HBM) today released its ann... READ MORE

Strategic acquisition of an established operating gold mine, loca... READ MORE

Cerro de Pasco Resources Inc. (TSX-V: CDPR) (OTCQB: GPPRF) (FRA: ... READ MORE

The Garneau Titanium Project Features Ilmenite-Rich Boulder with ... READ MORE

ValOre Metals Corp. (TSX‐V: VO) (OTCQB: KVLQF) (Frankfurt: KEQ0... READ MORE