American Lithium Corp. (TSX-V:LI) (NASDAQ:AMLI) (Frankfurt:5LA1) is pleased to announce the results of its maiden Preliminary Economic Assessment for the Tonopah Lithium Claims project located in the Esmerelda lithium district northwest of Tonopah, Nevada. This independent PEA was completed jointly by DRA Global and Stantec Consulting Ltd. and demonstrates that the TLC project has the potential to become a substantial, long-life producer of low-cost lithium carbonate with the potential to produce either battery grade LCE or lithium hydroxide. The PEA base case envisions an initial 4.4 Million tonnes per annum processing throughput expanding to 8.8Mtpa. The PEA alternative case is identical, but with added production of high purity magnesium sulfate as a by-product over life of operations. Unless otherwise stated, all dollar figures are in US currency.

TLC PEA Highlights (Base Case – Ramp-up Production Li only production):

Simon Clarke, CEO of American Lithium, states, “We are extremely pleased to announce a very robust maiden PEA for TLC. Our team has worked hard and spent considerable time getting an in-depth understanding of TLC mineralization and the best way to recover high purity lithium utilizing conventional processing methods with the latest techniques and best in class plant and equipment. A significant portion of the processing work has been done to pre-feasibility levels as we believe this will help us move quickly through the next phases of development. At 99.4% LCE purity, TLC offers the capability to produce either battery grade lithium carbonate or hydroxide with minimal additional refining.

In this PEA, we showcase a long mine-life utilizing only the highest-grade sections of the deposit, with the potential for additional production ramp-up and mine life utilizing our mid-grade and lower grade sections. Not only are the economics very strong for high purity lithium production, but TLC also has the potential to produce high purity magnesium sulfates as by-products for agriculture and other end uses. As shown in the PEA, even assuming conservative pricing, these by-products can add significant economic value. At the same time, we have focused our work on ensuring we continue to minimize environmental impacts and water usage in the mining, processing and production of lithium from TLC.”

TLC PEA Highlights (Alternate Case – Ramp-Up Production Li + Magnesium Sulfate production):

Mine Life & Production

Table 1 – TLC Project PEA Key Highlights

| Description | Units | Base Case | Alternate Case |

| LCE Selling Price | $/tonne | $20,000 | $20,000 |

| Life of Mine | years | 40 | 40 |

| Processing Rate P1 / P21 | ROM Mtpa | 4.4 / 8.8 | 4.4 / 8.8 |

| Average Throughput (LOM) | tpa | 8,112,415 | 8,112,415 |

| LCEProduced (average LOM)1 | tpa | 38,157 | 38,157 |

| P1 LCE Production (steady state) | tpa | 24,000 | 24,000 |

| P2 LCE Production (steady state) | tpa | 48,000 | 48,000 |

| LCE Produced (total LOM)1 | tonnes | 1,462,913 | 1,462,913 |

| Unit Operating Cost (OPEX) LOM2 | $/LCE tonne | 7,443 | 817 |

| MgSO4 Produced (average LOM)1 | tpa | n/a | 1,663,213 |

| MgSO4 Selling Price | $/tonne | n/a | 150 |

| Gross Revenue incl. Power & MgSO4 Credits | $ B | 29.7 | 39.4 |

| Capital Cost (CAPEX)3 P1 | $ M | 819 | 827 |

| Capital Cost (CAPEX)3 LOM | $ M | 1,431 | 1,439 |

| Sustaining Capital Costs (undiscounted) | $ M | 792 | 763 |

| Project Economics | |||

| Pre-tax: | |||

| Net Present Value (NPV) (8%) | U$ M | 3,642 | 6,056 |

| Internal Rate of Return (IRR) | % | 28.8 | 38.6 |

| Initial Payback Period (undiscounted) | years | 3.6 | 3.6 |

| Average Annual Cash Flow (LOM) | $ M | 435 | 684 |

| Cumulative Cash Flow (undiscounted) | $ M | 16,147 | 25,860 |

| After-tax:4 | |||

| Net Present Value (NPV)8%) Post-Tax | $ M | 3,261 | 5,157 |

| Internal Rate of Return (IRR) Post-Tax | % | 27.5 | 36.0 |

| Payback Period (undiscounted) | years | 3.8 | 3.7 |

| Average Annual Cash Flow (LOM) | $ M | 396 | 591 |

| Cumulative Cash Flow (undiscounted) | $ M | 14,617 | 22,219 |

Notes:

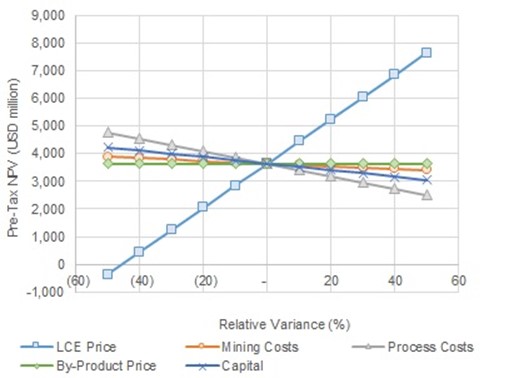

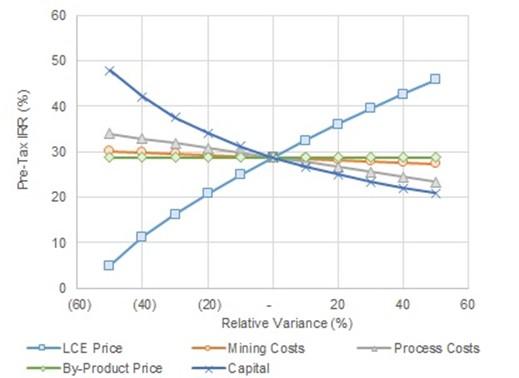

Sensitivities

The project is most sensitive to LCE price and process costs, but relatively far less sensitive to capital costs and mining costs, in descending order of affect (see Table 2, and Figures 1 and 2, below).

Table 2 – TLC Project Metal Pricing NPV8% and IRR Sensitivity

| Sensitivity ($)/t | -30% | -20% | -10% | Base Case $20,000/t |

10% | 20% | 30% |

| Pre-tax NPV8% (millions) | $1,243 | $2,042 | $2,842 | $3,641 | $4,441 | $5,240 | $6,040 |

| Pre-tax IRR (%) | 16.3 | 20.7 | 24.9 | 28.8 | 32.5 | 36.0 | 39.4 |

Figure 1 – Base Case Pre-Tax NPV8 Sensitivity Graph

Figure 2 – Base Case Pre-Tax IRR Sensitivity Graph

Mining

Based on the analysis completed by Stantec, the TLC Project is highly amenable for development by conventional open pit truck and shovel operation. The Base Case and Alternative Case have identical LOM production plans and schedules.

Table 3 – Mining Rates

| Parameter | Unit | Value |

| Mine Production Life | Years | 40 (includes 2-year production ramp up)1 |

| Material mined | Mt | 607 |

| ROM head grade to beneficiation | ppm Li | 1400 |

| Head Grade to Leach | ppm Li | 2000 |

| Recovered LCE | LOM Mt | 1.41 |

| Waste | LOM Mt | 292.5 |

| Total Mineralize Material throughput | LOM Mt | 315.3 |

| Strip Ratio (LOM) | (tw:to) | 0.93 |

Table 4 – Detailed Capital Cost Estimates:

| Capital Costs | Phase 1 |

Phase 2 |

LOM |

| ($ millions) | |||

| Mining (pre-strip and capital) | 56.3 | – | 56.3 |

| Processing plant – Direct costs | 424.5 | 228.8 | 653.3 |

| Processing plant/mine – Infrastructure | 45.9 | sustaining | 45.9 |

| Tailings & bulk infrastructure1 | 49.8 | sustaining | 49.8 |

| Total Direct Costs | 576.5 | 228.8 | 805.3 |

| Total Indirect Costs (Process Plant)2 | 181.9 | 316.8 | 498.7 |

| Contingency (Process Plant)10% | 60.6 | 54.7 | 115.3 |

| Closure Costs (captured in sustaining) | – | – | 25 |

| TOTAL – Li Only Base Case | 819.0 | 600.3 | 1,431 |

| Added Plant Capex for MgSO4 Production | 23.8 | 23.8 | 47.6 |

| TOTAL – Li + MgSO4 (includes tailings savings) | 827.0 | 1,439 | |

| Sustaining Capital Costs – Li only | – | – | 765.5 |

| Sustaining Capital Costs – Li + MgSO4 | – | – | 735.9 |

Flat 24,000 t LCE Production Scenarios

As part of the PEA modeling and design work, DRA Global and Stantec were also requested to evaluate flat 24,000 t/year LCE production scenarios without any production ramp-up using the identical 1,400 ppm Li feed scenario. The flat scenarios both have 20 years of mining followed by processing of stockpiled material for Years 21 to 36.

The two additional scenarios are as follows:

|

Table 5 – Capital and Operating Cost Estimates |

||||

| Case | Initial Capital (millions US$) |

LOM Capital (millions US$) |

US$/t LCE with power credit |

US$/t LCE with MgSO4 credit |

| Base Case | 819 | 1431 | 7429 | – |

| Alternate Case | 827 | 1439 | 7429 | 843 |

| Case 3 | 813 | 813 | 7543 | – |

| Case 4 | 822 | 822 | 7543 | 1,330 |

Table 6 – Financial Model Estimate Results Comparison

| Recovered LCE |

Recovered MgSO4 |

Pre-Tax Comparison |

||

| Case | t/a average | kt/a average | NPV (M US$) | IRR (%) |

| Base Case | 38,157 | 0 | $3,629 | 28.8% |

| Alternate Case | 38,157 | 1,681 | $6,030 | 38.6% |

| Case 3 | 21,930 | 0 | $2,136 | 27.5% |

| Case 4 | 21,930 | 909 | $3,592 | 38.2% |

Qualified Persons

Joan Kester, PG and Derek Loveday, P. Geo. of Stantec Consulting Ltd., Independent Qualified Persons as defined by National Instrument 43-101 Standards of Disclosure for Mineral Projects, have prepared or supervised the preparation of, or have reviewed and approved, the scientific and technical data pertaining to the Mineral Resource estimates contained in this release.

Satjeet Pander, P.Eng. and Sean Ennis, P.Eng of Stantec Consulting Ltd., Independent Qualified Persons as defined by NI 43-101, have prepared or supervised the preparation of, or have reviewed and approved, the scientific and technical data pertaining to mining, mine scheduling, and tailings management contained in this release.

John Joseph Riordan, BSc, CEng, FAuslMM, MIChemE, RPEQ, of DRA Pacific (Pty) Ltd., and Valentine Eugene Coetzee, BEng, Meng, P.Eng. of DRA Projects SA Pty Ltd., Independent Qualified Persons as defined by NI 43-101, have prepared or supervised the preparation of, or have reviewed and approved the scientific and technical metallurgical information and financial modelling results contained in this news release.

Mr. Ted O’Connor, P.Geo., Executive Vice President of American Lithium, and a Qualified Person as defined by National Instrument 43-101 Standards of Disclosure for Mineral Projects, has also reviewed and approved the scientific and technical information contained in this news release.

In accordance with NI 43-101, the Company intends to file the completed technical report on the PEA under the Company’s profile on SEDAR (www.sedar.com) and on the Company’s website within 45 days from the date of this news release.

About DRA Global Limited (ASX: DRA | JSE: DRA), as lead engineer, is a diversified global engineering, project delivery and operations management group headquartered in Perth, Australia, with an impressive track record completing over 300 unique projects worldwide spanning more than three decades. Known for its collaborative approach and extensive experience in project development and delivery, as well as turnkey operations and maintenance services, DRA Global delivers optimal solutions that are tailored to meet clients’ needs. DRA Global, through its subsidiary, DRA Met-Chem, has a team of lithium process and metallurgical experts that identify the process requirements through flowsheet development and process equipment is selected to minimize costs and ensure plant efficiency.

About Stantec Consulting Ltd., a full-service engineering and consulting firm, has extensive experience in surface mineable stratiform deposits in North American and internationally. Stantec has been involved in the evaluation and design of several lithium projects with services spanning from environmental studies, geological modeling, resource and reserve estimates, mining engineering, hydrology and hydrogeology, geotechnical engineering, and tailings, waste, and water management facility design. The company specializes in helping mining companies to reach their net zero mining goals.

About Mining Tax Plan LLP. Mining Tax Plan LLC specializes in U.S. federal and state income taxation including foreign income taxation of precious metal, non-metallic ores, coal and quarry mining companies. They have extensive experience with extractive and natural resource industries and have provided consulting services to clients in such areas as mergers and acquisitions, corporate distributions, restructuring and foreign investment. In addition, they specialize in state mineral property and severance taxes in Alaska, Arizona, California, Colorado, Idaho, Montana, Nevada and Utah.

About American Lithium

American Lithium, a member of the TSX Venture 50, is actively engaged in the development of large-scale lithium projects within mining-friendly jurisdictions throughout the Americas. The Company is currently focused on enabling the shift to the new energy paradigm through the continued development of its strategically located TLC lithium claystone project in the richly mineralized Esmeralda lithium district in Nevada, as well as continuing to advance its Falchani lithium and Macusani uranium development-stage projects in southeastern Peru. Both Falchani and Macusani have been through robust preliminary economic assessments, exhibit strong significant expansion potential and enjoy strong community support. Pre-feasibility work has now commenced at Falchani.

Namibia Critical Metals Inc. (TSX-V: NMI) (OTCQB: NMREF) is pleased to announce that Japan Organizat... READ MORE

Eldorado Gold Corporation (TSX: ELD) (NYSE: EGO) today reports the Company’s financial and operati... READ MORE

DPM Metals Inc. (TSX: DPM) (ASX: DPM) announced its operating and financial results for the second q... READ MORE

IMC Rare Earths Ltd, a company focused on the mineral exploration and development of magnet rare ear... READ MORE

Fairchild Gold Corp. (TSX-V: FAIR), is pleased to announce the closing, on July 29, 2026, of its pre... READ MORE