I will dive into the copper market in some depth next week but for now I can’t help but share a few of the key conclusions from two big recent copper outlook reports. One, from the Bank of Montreal, assessed the state of supply and demand. The other, from CitiBank, looked at 18 major copper miners in terms of free cash flow and what they might do with their money.

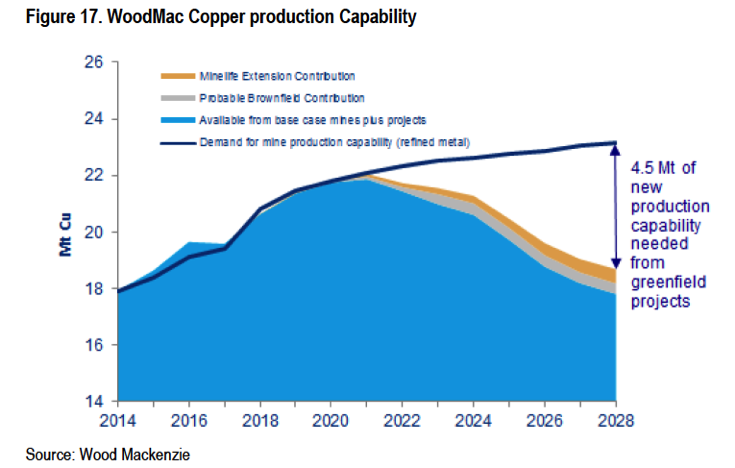

The reports agreed on the big picture: the copper market is heading towards a serious deficit. This is a market that churns through some 21 million tonnes of metal annually…and from 2025 to 2030 it will be short 5 million tonnes of copper annually.

Five million tonnes! That’s 10 billion pounds and a quarter of the entire market. It is a staggering deficit and one that will require immense buildout to meet.

Enter the Citi report. One conclusion: assuming the need for a 15% internal rate of return (after accounting for country risk), Citi sees the need for copper prices of at least US$3.60 per lb. to incentivize the greenfield development necessary to close the supply gap.

OK, so there is strong fundamental support for copper prices to continue rising. On the flip side, prices are already up 24% in a year or 55% in two years. And with stronger prices following years of cost cutting, copper miners are making good cash right now.

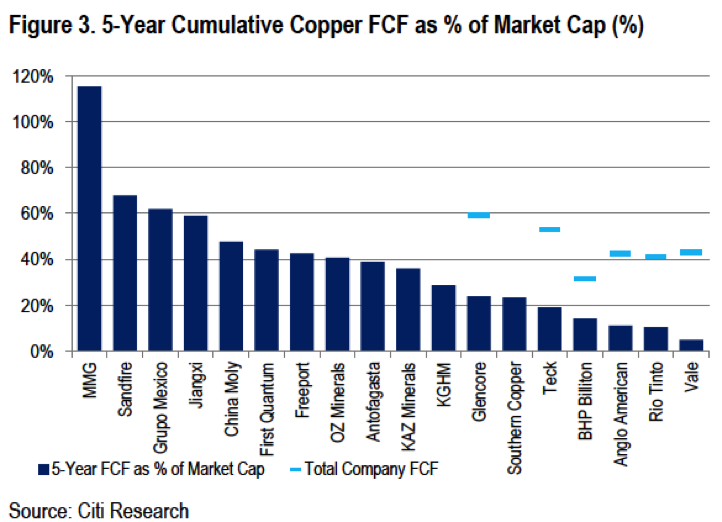

Citi’s deck of 18 major copper miners is expected to generate US$125 billion in free cash flow from 2018 to 2022. That’s a lot of money – and it comes against low market valuations. The standout in the group, for example, is MMG, which is expected to generate 115% of its current market cap in free cash flow within a few years.

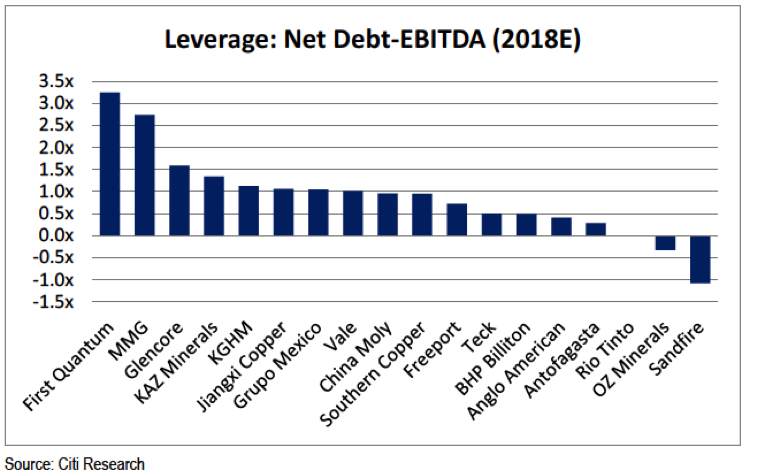

OK, so they’ll be rolling in cash. The obvious question is: what will they do with it all? There are four categories:

Lots of money means lots of potential. Sure, Citi sees limited deals among its deck of miners, but that just means those miners will have to look at smaller companies for projects. And there are some available – medium to large copper assets that are largely derisked and will get bought as this cash flow machine really gets going.

The huge supply gap also means strong new discoveries will attract a lot of attention. It isn’t really happening yet – copper discoveries aren’t catching attention like gold discoveries are – but that time is nigh.

Silver Mountain Resources Inc. (TSX-V: AGMR) (OTCQB: AGMRF) is ... READ MORE

Mandalay Resources Corporation (TSX: MND) (OTCQB: MNDJF) announce... READ MORE

Collective Mining Ltd. (TSX: CNL) (OTCQX: CNLMF) (FSE: GG1) is pl... READ MORE

Significant copper and molybdenum intersections include: HM19: 11... READ MORE

Red Pine Exploration Inc. (TSX-V: RPX) (OTCQB: RDEXF) is pleased ... READ MORE